When Tola, a fashion entrepreneur in Lagos, tried to pay her supplier in Nairobi, she expected the transaction to be as smooth as ordering an Uber.

Instead, she had to convert naira to dollars, find a platform that supports Kenyan shillings, and pay a fee that could buy her enough fabric for five dresses. The payment took three days. Her supplier waited, her production halted, and a client order slipped through the cracks.

Multiply Tola’s experience by millions of entrepreneurs across 54 countries, and you begin to understand why intra-African trade remains stubbornly low despite decades of integration rhetoric. The cost is measured in lost opportunities, failed businesses, and an economic integration that exists more in PowerPoint presentations than in practice.

Despite the fintech buzz sweeping across Africa, the simple act of moving money across borders remains slow, expensive, and unreliable. And while flashy apps promise to “revolutionise finance,” the root problem remains untouched: Africa’s financial systems are fragmented, and that fragmentation is costing the continent $5 billion annually in unnecessary payment costs.

The Cross-Border Payment Landscape: Broken by Design

Africa trades with itself far less than any other region in the world. Intra-African trade accounts for just 15% of total exports, compared to 60% in Europe and 38% in North America. Meanwhile, China-Africa trade has hit $295 billion annually, exceeding total intra-African trade of $175 billion.

One reason for this disparity? Moving money between African countries is painfully inefficient. There are over 40 currencies on the continent, most of which aren’t freely convertible.

Payments often route through intermediary banks in the U.S. or Europe before returning to the continent.

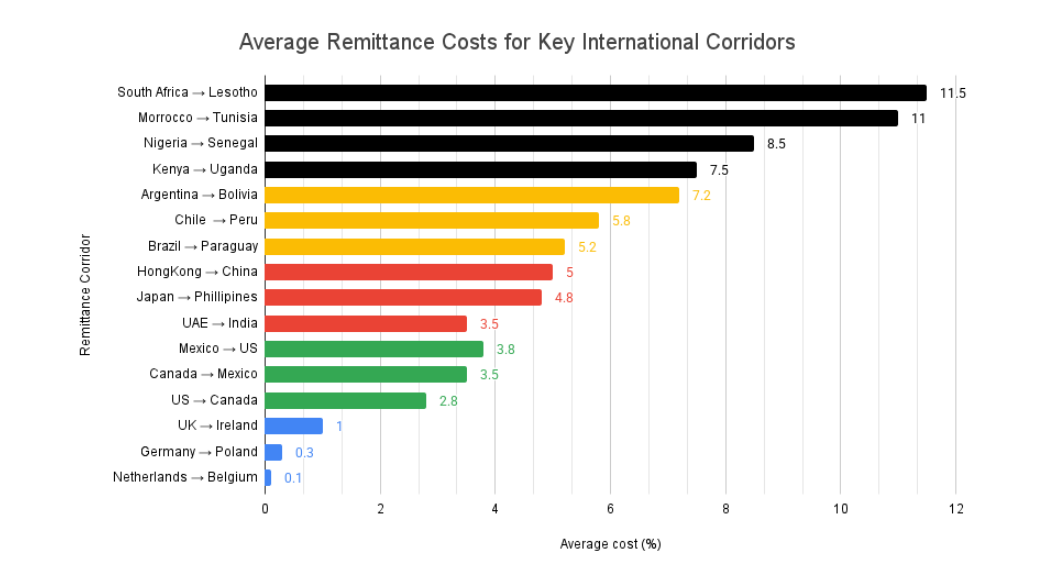

That journey is expensive as shown in Figure 1 which details the average remittance cost per payment corridor for each continent.

This acts as a tax on growth, which is why about 75% of African trade happens through informal channels, specifically to avoid these costs, creating a massive underground economy. According to UNCTAD’s 2023 Economic Development in Africa Report, inadequate payment systems are a key factor in the continent’s trade underperformance.

The Mobile Money Paradox

Africa leads the world in mobile money innovation. Kenya has 77 million mobile money accounts for a population of 56 million.

According to the newly released State of the Industry Report on Mobile Money (SOTIR) 2025 by GSMA, a global organisation that unifies the mobile ecosystem, sub-Saharan Africa (SSA) recorded 1.1 billion of the 2 billion mobile money accounts registered globally as of 2024, yet these systems remain isolated.

While you can send money instantly within countries, cross-border transactions remain costly and cumbersome.

This is the mobile money paradox: a continent that pioneered financial inclusion through mobile wallets still struggles with regional financial integration.

Domestic transactions are fast, cheap, and widespread. But the moment money needs to cross a border, the system breaks down due to fragmentation thereby leading to an expensive and inefficient transaction.

We need to connect the pipes so that Africa’s mobile money revolution can grow from a local success into a truly continental one.

Fintechs Are Innovating, But Reach Is Limited

Startups like Flutterwave, Chipper Cash, Nala, and Eversend offer wallet-based cross-border payments. However, many operate in closed systems. Funds often can’t be withdrawn into local bank accounts, and FX rates remain inconsistent.Some fintechs also hesitate to expand due to regulatory uncertainty, capital controls, and compliance hurdles.

Underground alternatives on the other hand are flourishing. Nigeria alone accounts for about 40% of Sub-Saharan Africa’s stablecoin inflows with latforms such as Juicyway processing over $1.3 billion in stealth cross-border transactions, driven purely by demand.

The Real Villain: Fragmentation

Each country has its own licensing, Know Your Customer (KYC), Anti-Money Laundering (AML), and Foreign Exchange (FX) rules. Opening accounts in Ghana, Kenya, or South Africa often requires country-specific documentation, local guarantors, and additional clearance. Nigeria’s multiple exchange rates and currency restrictions worsen the chaos.

Compare this to Europe’s SEPA. These systems demonstrate what happens when you build infrastructure first and compete second.

PAPSS and AfCFTA: Promise Without Speed

The Pan-African Payment and Settlement System (PAPSS) is Africa’s boldest attempt yet at breaking the cross-border payments bottleneck. Developed by Afreximbank in collaboration with the African Union (AU) and launched in 2022, PAPSS allows businesses and individuals in participating African countries to pay each other directly in their local currencies; no need to route payments through the U.S. dollar or euro.

Here’s how it works: when a buyer in Ghana initiates a payment to a supplier in Nigeria, PAPSS instantly converts Ghanaian cedis to Nigerian naira using real-time exchange rates negotiated between central banks.

The transaction clears locally, reducing reliance on foreign correspondent banks and cutting transaction costs and time.

In fact, over 115 commercial banks and several central banks have already joined the network. In one notable case, a Ghanaian company successfully paid a Nigerian partner in local currency in under five minutes.

So, why isn’t PAPSS everywhere yet?

Because solving a technical problem is not the same as solving a systemic one.

- Regulatory uncertainty: Each country operates under its own regulatory framework. Some central banks are still working through how PAPSS fits into their compliance, capital control, and anti-money laundering regimes. Without clear rules or standardised legal frameworks, many banks are adopting a “wait and see” approach.

- Liquidity concerns: For PAPSS to work smoothly, central banks need to maintain enough local currency reserves to settle transactions in real time. But volatile exchange rates, fluctuating reserves, and inflation risks make this a delicate balancing act, especially in countries already struggling with monetary stability.

- Legacy systems: Many African banks still operate on outdated core banking systems that don’t integrate easily with new platforms like PAPSS. The technical upgrades required to connect fully are costly and time-consuming.

- Awareness gap: A significant number of African businesses—especially small and medium enterprises (SMEs)—have never heard of PAPSS. The product has had limited promotion outside of pilot countries, and adoption strategies have been largely top-down, missing grassroots financial ecosystems that power most trade.

- Incentive mismatch: Some banks benefit from the status quo. They earn fees from foreign currency conversions and maintain profitable correspondent banking relationships abroad. PAPSS threatens those margins, so there’s little internal motivation to push adoption.

PAPSS was designed to be the financial infrastructure supporting the African Continental Free Trade Area (AfCFTA), which is Africa’s most ambitious economic integration project to date. AfCFTA aims to remove tariffs on 90% of goods, ease the movement of people and services, and boost intra-African trade by as much as $50–70 billion by 2040.

Trade liberalisation without payment liberalisation is like building roads with no vehicles. Businesses might have legal permission to trade, but without affordable and fast cross-border payment systems, the potential gains remain locked up.

AfCFTA and PAPSS are two sides of the same coin; one sets the policy, the other enables execution. But for PAPSS to scale, political will must match technical readiness.

That means central banks must fast-track integration, governments must legislate for interoperability and transparency, and banks must be incentivised—or compelled—to onboard. Most importantly, the private sector needs to be educated and empowered to adopt the platform at scale.

The Missing Piece: Shared Infrastructure and Political Will

Every time a payment between African countries gets routed through London, New York, or Frankfurt, it’s a loss of control. Africa pays in fees, speed, and sovereignty. If intra-African trade is to become a reality, not just a policy paper, then payments infrastructure must evolve from fragmented and foreign-dependent to interoperable and African-owned.

Right now, we don’t just have a payment gap. We have a coordination gap. Building the technical rails is only half the job.

The harder challenge is aligning governments, regulators, and private sector players around shared rules, common standards, and mutual trust. Without that alignment, even the best technology will gather dust.

Here’s what needs to happen:

1. Regulatory Harmonisation

Each African country has its own approach to KYC (Know Your Customer), AML (Anti-Money Laundering), and payment licensing. This makes cross-border compliance a nightmare for banks and fintechs. We need a pan-African regulatory framework that defines:

- Standardised onboarding and verification protocols

- Shared risk assessment models

- Data-sharing agreements between regulators

A unified set of rules would reduce friction and speed up onboarding, especially for smaller players that can’t afford complex compliance operations.

2. FX Reform and Local Liquidity Pools

A significant reason many payments leave the continent is that they need to be converted into a “hard” currency first, typically USD or EUR. Central banks should consider:

- Creating regional FX liquidity pools backed by Afreximbank

- Publishing real-time exchange rates

- Enabling local settlement between trusted institutions, even in thinly traded currencies

This will reduce volatility and make local currency settlements more appealing.

3. Public-Private Collaboration

Governments can’t build this alone. They need fintechs, telecoms, and banks to join forces in designing and rolling out solutions that actually meet the needs of African traders. That means:

- Incentivising private sector R&D through grants and tax relief

- Opening regulatory sandboxes for experimentation

- Fast-tracking licenses for fintechs solving cross-border problems

Innovation tends to happen at the edge, not the centre. Smart partnerships can bridge the gap.

4. PAPSS Expansion Through Awareness and Mandates

It’s not enough for PAPSS to exist; it needs to become the default. That requires a coordinated campaign across all levels:

- Central banks mandating its use for eligible cross-border public sector payments

- Governments adopting it for procurement and aid disbursements

- Chambers of commerce and trade associations promoting it to their members

- Training banks, MSMEs, and payment operators on how and why to use it

PAPSS adoption must be pushed, not just permitted.

5. Real-Time Data Interoperability

African countries need data interoperability. That includes APIs that allow different banks and fintechs to “talk” to each other securely in real time. Without this, cross-border transactions will always feel clunky and delayed.

Open banking frameworks and shared infrastructure layers (like digital identity, credit registries, and fraud detection systems) can close the loop.

The Stakes Couldn’t Be Higher

Tola and millions like her deserve better. If payment barriers fall, Africa’s income could rise by $450 billion by 2035, according to the World Bank.

We have PAPSS, mobile money, and fintech platforms. What we need is the political will to make them work together. Let’s move beyond pilots. Let’s move money. The infrastructure exists. The demand is massive. The only question is whether we will use it before the world leaves us behind.

*Motunrayo Koyejo is a software engineer specialising in fintech solutions for emerging markets. With a passion for leveraging technology to drive financial inclusion, she contributes insights to Africa’s digital transformation. She currently works as a senior software engineer at Cowrywise

Insightful, Thank you.