Highlights

Operating key performance indicators (KPIs)

- Airtel Africa: Total customer base grew by 9.1% to 151.2 million. The penetration of mobile data and mobile money services continued to rise, driving a 22.4% increase in data customers to 62.7 million and a 19.5% increase in mobile money customers to 37.5 million.

- Constant currency ARPU growth of 10.0% was primarily driven by increased usage across all segments.

- Mobile money transaction value increased by 41.3% in constant currency, with Q3’24 annualised transaction value of $116bn in reported currency.

Financial performance

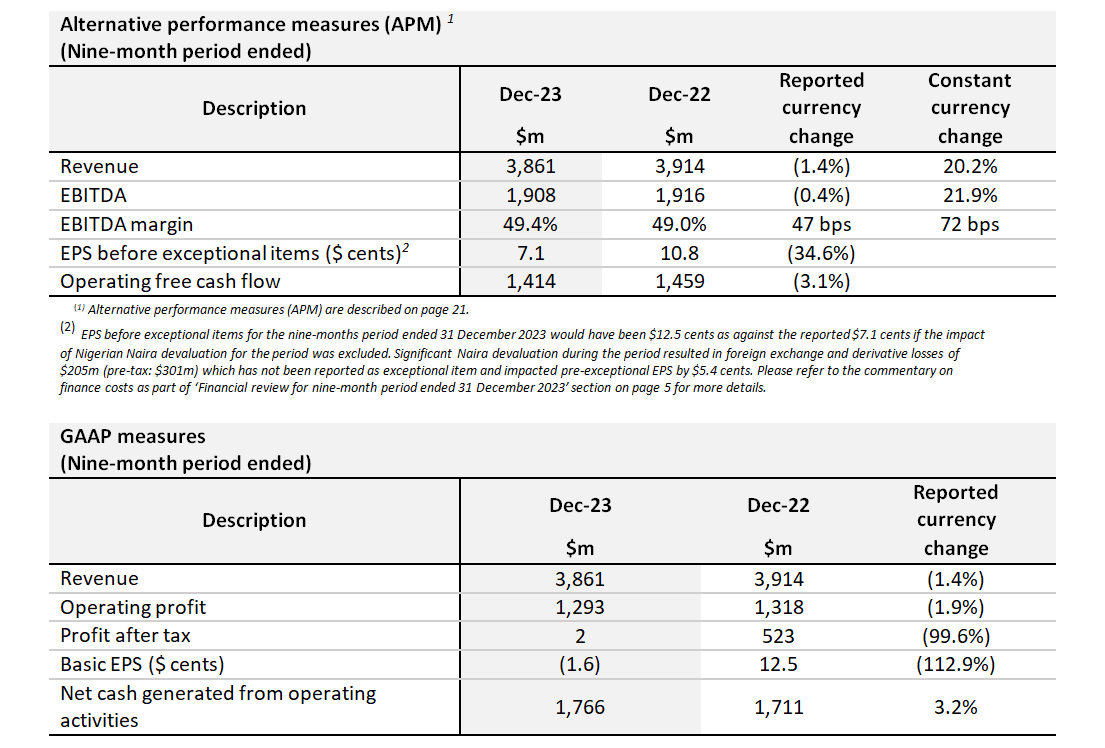

- Revenue in constant currency grew by 20.2%, with Q3’24 growth accelerating to 21.0%. Reported currency revenues declined by 1.4% to $3,861m. In Q3’24, reported currency revenues declined by 8.3% as currency devaluation (primarily the Nigerian naira devaluation) continued to impact reported revenue trends.

- All segments continued to deliver double-digit constant currency growth. Across the Group mobile services revenue grew by 18.6% in constant currency, driven by voice revenue growth of 11.2% and data revenue growth of 28.5%. Mobile money revenue grew by 31.8% in constant currency.

- Constant currency EBITDA increased 21.9%, with Q3’24 EBITDA growing 23.3%. The EBITDA margin of 49.4% increased 72bps over the prior period despite foreign exchange headwinds and inflationary pressure. Reported currency EBITDA declined by 0.4% to $1,908m, with Q3’24 EBITDA 8.3% lower as currency headwinds continued to impact reported trends.

- Profit after tax was $2m in the period, primarily impacted by significant foreign exchange headwinds, particularly the $330m exceptional loss after tax following the devaluation of the Nigerian naira in June 2023 and the Malawian kwacha in November 2023 after the structural changes in their respective FX markets. The Nigerian naira devalued further in Q3’24, resulting in a $140m derivative and foreign exchange losses net of tax, which is not treated as an exceptional item.

- EPS before exceptional items was 7.1 cents, a decline of 34.6%. Basic EPS at negative (1.6 cents) compares to 12.5 cents in the prior period, impacted by the significant derivative and foreign exchange losses as explained above.

Capital allocation

- Capex of $494m was 8.2% higher compared to the prior period. Capex guidance for the full year remains between $800m and $825m as we continue to invest for future growth.

- Leverage of 1.3x in December 2023, improved from 1.4x in the prior period. The remaining debt at HoldCo is $550m, falling due in May 2024. Cash at the HoldCo was $560m at the end of the period and the Group is expecting to fully repay the HoldCo debt when due.

- In light of the Holdco cash accretion and where leverage is today, and in view of the consistent strong operating cash generation of the Company, the Board intends to launch a share buy-back programme of up to $100m, starting early March 2024 over a 12-month period.

Sustainability strategy

- Airtel Africa ‘s landmark five-year $57m partnership with UNICEF has been launched across 10 of our markets providing access to educational resources, free of charge, on our way to transforming the lives of over one million children through our educational programmes by 2027.

- In November 2023 Airtel Africa launched its Scope 3 strategy which focuses on an ongoing engagement programme with the top tier partners and suppliers, ensures a regular flow of information and enables the Group monitor their impact on the environment.

[Abridge Report]