The need to strengthen global frameworks, increase the digitalization of financial services at lower operational costs, and upgrade fintech services beyond mobile banking to include lending, insurance, investment, personal finance management, and other services has led to a significant increase in the number of fintech businesses in Nigeria over time.

In Nigeria, there were more than 100 fintech startups operating in the mobile money, credit, e-payment, and e-collection sectors as of 2018.

With Interswitch, which received a valuation of $1 billion thanks to a $200 million investment from Visa, Nigeria officially acknowledged its first fintech unicorn in 2019.

Just five years after Paystack was formed, in 2020, Stripe, a US-based financial services firm, decided to buy it for $200 million.

A Nigerian startup raising $10 million was unusual ten years ago. The nation’s unicorn fintech companies are now worth almost as much as its banks. OPay is worth over $2 billion, Interswitch is worth over $1 billion, and Flutterwave was valued at $3 billion last year.

The fact that fintechs have achieved remarkable success is not surprising. They are well-positioned to address customer financial management pain points by offering rapid loans, inexpensive payments, and flexible savings and investing options.

Within the financial services business, financial technology has been reemerging and rapidly evolving for some time. Given its potential to completely transform how individuals save, borrow, and spend money, fintech is attracting the attention of investors and the government. It is probably this attention that has drawn several fees to startups operating in the fintech space.

Intense Attention

The Central Bank of Nigeria (CBN), which gets its regulatory authority from the Banks and Other Financial Institutions Act, 2020 (BOFIA), is the primary regulator of financial technology businesses in Nigeria.

Also read: Nigeria’s SEC Grants Volition Cap License to Kickstart Fund Management

The Nigerian Communication Commission, established under the Nigerian Communication Act of 2003, the Securities and Exchange Commission (SEC), established under the Investment and Securities Act of 2007; the National Insurance Commission, and the Corporate Affairs Commission (CAC), established under the CAMA 2020, are among the other regulators.

Due to variations in legislative frameworks and market conditions, operating costs for fintech firms vary between African nations. It is advised that Nigerian fintech innovators speak with local professionals and regulatory bodies to determine the costs associated with operating a fintech. However, I can give you several of them right here.

Regulatory costs: Different regulatory requirements, such as licensing fees, compliance charges, and capital adequacy criteria, are present in African countries for fintech enterprises. These expenses differ between countries and depend on the particular activities carried out by the fintech company.

Licensing: In order for fintech companies to legally operate, some African nations impose licensing fees. Depending on the government and the kind of fintech services provided, the fees might differ significantly, ranging from relatively small sums to more considerable sums.

Fintech companies frequently pay transaction fees for online payments, remittances, and other financial services.

These charges may vary depending on a number of variables, including the payment infrastructure, business relationships with banks or mobile network operators, and governmental rules governing online transactions.

Costs of compliance: Anti-money laundering (AML) and know-your-customer (KYC) laws must be complied with by fintech companies. Implementing systems for client due diligence, identification verification, and transaction monitoring, which can range in complexity and associated costs, can be one of these compliance costs.

Taxation: The respective African countries’ corporate income tax, value-added tax (VAT), and other charges may apply to fintech companies. Different jurisdictions may offer fintech companies different tax benefits and rates.

Milking the Fat Cow Through License

The expansion of the fintech sector has not been greatly facilitated by the Nigerian regulatory framework for financial technology. The value of mobile money transactions has increased dramatically during the last ten years.

As a result, in an effort to increase revenue in numerous African countries with high debt levels and declining tax revenues, mobile money transactions are now subject to levies. These are the Nigerian regulatory procedures for a number of fintech operation licenses:

Processing and switching: Here, financial transaction processing is offered by fintech businesses. The registration of the business with the Corporate Affairs Commission is the first step in getting this license.

- A switching and processing company must have a minimum share capital of ₦2 billion ($4 million).

- An application must be made to the CBN with all accompanying documents. The application fee is ₦100,000, while the licensing fee is ₦1 million.

Mobile Money Operators: Mobile money providers can conduct financial transactions using their mobile phones. By using unique USSD codes on their phone network, they enable client transactions. Obtaining this license entails the following steps:

- A mobile money operator’s minimum share capital is 2 billion won ($4 million).

- The CBN must receive an application and all supporting documentation.

- The licensing price is ₦1 million, whereas the application fee is ₦100,000.

Providers of payment terminal services (PTSPs): Fintech organizations with a license to deploy, manage, and maintain POS terminals are known as payment terminal service providers. To receive a PTSP license, follow these steps:

- Registration of the company with the Corporate Affairs Commission

- The minimum share capital of a Payment Terminal Services Provider company is ₦100 million ($200,000)

- An application must be made to the CBN with all accompanying documents. The application fee is ₦100,000, while the licensing fee is ₦1 million.

Payment Solution Service Providers (PSSP): Payment solution service providers are fintech companies that act as fund collectors on behalf of their customers. They serve mostly the interests of merchants by enabling payment through the web. The procedure for obtaining a PSSP license is:

- Registration of the company with the Corporate Affairs Commission

- The minimum share capital of a Payment Solution Service Provider company is ₦100 Million ($200,000)

- An application must be made to the CBN with all accompanying documents. The application fee is ₦100,000 while the licensing fee is ₦1 million.

African fintech firms now face many perplexing and restrictive rules, and many have been forced to forge strategic alliances with established players. Prior to recently, central banks had permitted these fintechs to function without licenses.

Also read: NCS Cautions Against Hasty Passage of NITDA Bill

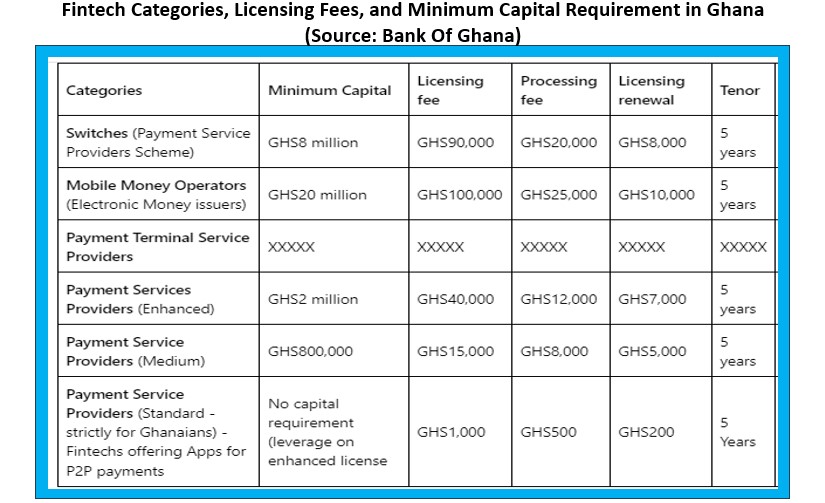

According to Ghana’s Payment Systems and Services Act, 2019 (Act 987), a license must be applied for in the prescribed manner to operate a payment service business or issue electronic money.

The license will then be granted after governance arrangements, reasonable fees, technology, security, controls, adherence to the universal consumer protection principles, and a suitable complaint procedure have been met.

Tax and License Paradox

It is important to pay close attention to the costs that fintech businesses must bear as African nations develop their financial services. It would seem that regulators prioritize getting paid over promoting innovation in the financial services industry.

Last year, a fee on electronic transfers, including mobile money transactions, was adopted in a number of African nations, including Ghana, Cameroon, Uganda, Tanzania, the Congo Republic, Zimbabwe, Ivory Coast, and Kenya. Low-income, fee-sensitive individuals as a result were fast to switch back to cash-based payments.

According to polls, there are fewer active agents and fewer transactions involving agents in Ghana. Following the introduction of a mobile money tax in Tanzania in July, peer-to-peer transactions decreased there by 38%, from 30 million to 18 million per month.

Africa’s ambition to go cashless is obviously at odds with its determination to charge heavy costs for digital transformations.

Cash still prevails, as seen by the latest complaints about the lack of currency in Nigeria. Authorities must support mobile or online banking by reducing fees on all fronts if it is to become the norm in the area. This encourages increased adoption while also allowing in more operators.