By: Fintech Association of Nigeria

Corporate governance exists regardless of whether an organisation pays attention to it or not. The key difference is that fintech companies with a good governance structure will be more sustainable in the long run, while customers and regulators will see right through the cracks of a fintech with poor corporate governance.

For better understanding of the concept, corporate governance can be defined as the set of rules, practices and guidelines with which an organisation uses to operate, control and manage its business.

The key principles of corporate governance are accountability, transparency, fairness, responsibility and last but not the least, risk management.

While adherence to corporate governance is a business-as-usual activity to banks who are often tightly regulated both locally and globally, fintechs have typically more latitude, especially when they are starting up.

Fintech companies are typically in the news for ground-breaking achievements such as investor funding, annual profits, rise in valuation or cross-border expansion.

Entrepreneurial and innovation biases, often predominant in founders, is often not backed up with same level of enthusiasm for governance.

Globally, some of the largest fintech companies have been called out recently for all the wrong reasons – ranging from financial misconduct to insider trading, to name just a few.

Given the exponential growth and investments into the fintech industry, investors, regulators and indeed customers are demanding governance practices and corporate governance in fintech has now become a critical success factor, beyond building a marketable product that scales to the unicorn status.

The most recent Africa Tech Venture Capital (VC) report released by Partech Africa revealed that in 2022, the African tech ecosystem raised US$ 6.5 billion in funding, representing a growth of 8% from the previous year.

The growing interest in the sector, and recent global crisis involving operators such as FTX has raised stakeholder interest in the affairs of fintech companies, demanding transparency and sound governance practices to ensure the sustainability of firms in the industry.

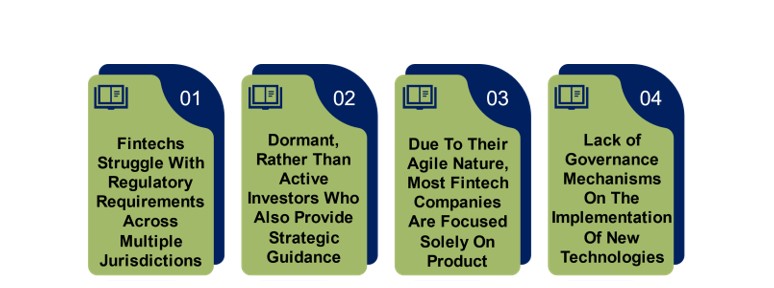

If the link between corporate governance and success is so clear, why are some fintech firms still experiencing gaps and, in some cases, unwilling to establish a robust governance structure? Our research has revealed four recurring challenges:

In a recent publication by Punch Newspaper, it was confirmed that an astounding number of Nigerian start-ups collapsed within the first five years due to their inability to operate clearly spelt-out corporate governance structures. Since we have identified the most common reasons why corporate governance often takes the back seat in fintech, we must also propose some steps that fintech firms can take in improving the governance culture. The steps include:

Notice that the importance of the Board of Directors keeps coming up when we look at ways to ensure sound governance. This goes to show that the subject matter must be owned at all levels within the organisation, and an effective Board ensures and follows up that this happens as there is no greater risk to an organisation’s survival than poor governance. This includes financial, legal and reputational harm.

Generally, a good Board of Directors is a balanced team with complementary skill sets and a culture that allows them to work together to make the most effective decisions. To maximise the efficacy of the board, fintech companies may do the following; clearly define roles and responsibilities, examine board structure, revise formal operating procedures, keep track of decisions and actions, evaluate board composition, understand board culture, and finally, the CEO should engage with board members.

To summarise, sound corporate governance in the fintech industry will establish direction for companies, encourage business integrity, promote financial viability and build trust with investors and the community. Corporate governance is a continuous process and gaps in enforcing it can no longer be ignored. The Nigeria Deposit Insurance Corporation (NDIC) has affirmed its supervisory role in ensuring financial system stability. The corporation is collaborating with regulators and other global stakeholders in order to develop supervisory measures, particularly for digital banks.

We want to hear your thoughts, how can fintech companies rise up to the corporate governance expectations placed on them? Comment below to continue the conversation.

Some existing regulations in corporate governance are: Guidelines on Mobile Money Services in Nigeria by the Central Bank of Nigeria(CBN), Guidelines for FinTech Regulatory Sandbox by the Securities and Exchange Commission (SEC), Guidelines for Data Protection Compliance in Nigeria by National Information Technology Development Agency (NITDA), Framework for the Provision of Value Added Services by Nigerian Communications Commission (NCC), Value Added Tax Act by Federal Inland Revenue Service (FIRS), NIBSS Industry Standards and Operating Guidelines by Nigeria Inter-Bank Settlement System (NIBSS).

In our next series on Building Resilience in Fintech Business, we will take a closer look at Risk Management and Compliance.

…Continue Reading HERE

Comments 1