Before we dive into this highly anticipated subject, let’s cover the basics. A cashless economy refers to an economic system based on digital payments and cash alternatives such as debit and credit cards, mobile and internet banking, as well as digital wallets.

According to Fintech Magazine, Sweden is currently the most cashless economy in the world, with many Swedish banks no longer accepting cash deposits, 32 Automated Teller Machines (ATMs) per 100,000 people and cash accounting for only 1% of all transactions.

ALSO READ: FinTechs are Important to Reducing Cash in Circulation – FG

As a result of this, Riksbank, Sweden’s Central Bank, can adequately account for the amount of money in circulation. By going completely cashless, the transfer of funds is seamless across the country, the risk of cash theft is mitigated and there is overall transparency and accountability across Sweden.

The Central Bank of Nigeria (CBN) first issued the framework for its cashless policy in 2012, to reduce the amount of physical cash in circulation, deepening financial inclusion by driving digital payments, reducing fraud and curbing cash-aided crimes such as terrorism financing, kidnapping, extortion, blackmail, and so on.

Today, the maximum weekly withdrawal limits for individuals and corporates across all channels are N500,000 and N5,000,000 respectively.

In an event where cash withdrawal exceeds these limits, a processing fee of 3% and 5% will be incurred for individuals and corporates, respectively. In addition, third-party cheques exceeding the sum of N100,000 are not eligible for over-the-counter (OTC) payment.

On the surface, a cashless economy in itself does not seem like a bad policy. Anyone who has been paying attention to the global payments trend knows that a cashless world looms and that it is only a matter of time till hard notes become obsolete or close enough.

To support this, Bain and Company report that 67% of global payments will be done digitally by 2025. Already, we are experiencing digital-only banks (neo-banks) and contactless payments with the help of smartphones and super-fast networks. We are also experiencing emerging digital trends such as the use of cryptocurrency for payments and settlements, which has inspired some central banks to pick up the innovator hat.

In October 2021, Africa’s first Central Bank Digital Currency (CBDC), the E-Naira, was born as part of the strategic drive away from cash. We once used gold bars, barter, ivory shells and coins as modes of payment, remember? The use of cash as a medium of exchange has been declining gradually for years.

The drive for a cashless economy at all costs by the CBN is strategic, however, the execution and results have been described by many pundits as suicidal.

The new naira notes became legal tender on 15th December 2022, after being unveiled the previous month by President Muhammadu Buhari and CBN Governor, Godwin Emefiele.

In an announcement that would reverberate through the whole country, over 200 million Nigerians were given just under two months, until 10th February 2023, to get with the status quo, even after a series of backlash and expressions of displeasure by the public.

The cash swap is being driven on steroids. This may be perceived to signal insensitivity and a lack of consideration of key stakeholders by the apex bank. A cashless policy should bring about greater ease and convenience of payments, but is the opposite effect materializing in Nigeria today?

Challenges with execution may be leading to the erosion of trust in the banking system, with merchants asking for cash payments despite empty ATMs, digital channels increasingly overwhelmed and POS charges inching towards 50%. When the United Kingdom issued new £20 and £50 notes, both the old and new pound sterling notes co-existed for about eighteen (18) months until naturally, the old notes were no longer in circulation, as the case should be.

The current predicament facing Nigeria can be likened to what happened in November 2016, when India introduced its demonetization policy to reduce the circulation of high denomination rupees, as well as to tackle corruption, tax evasion and other illegal activities.

Similarly, cash withdrawals from banks were restricted to 10,000 rupees (US$150) daily and 20,000 rupees (US$300) weekly.

The policy made it near impossible for Indians to access their hard-earned money for a long time, resulting in many controversies, deflated trust in the Indian government and an overarching negative economic impact.

India’s cashless policy was not successful because the challenges and concerns of the people such as preferences, economic development and technological advancement, were not adequately addressed. The same situation is being experienced in Nigeria today, with empty ATMs and exorbitant POS charges.

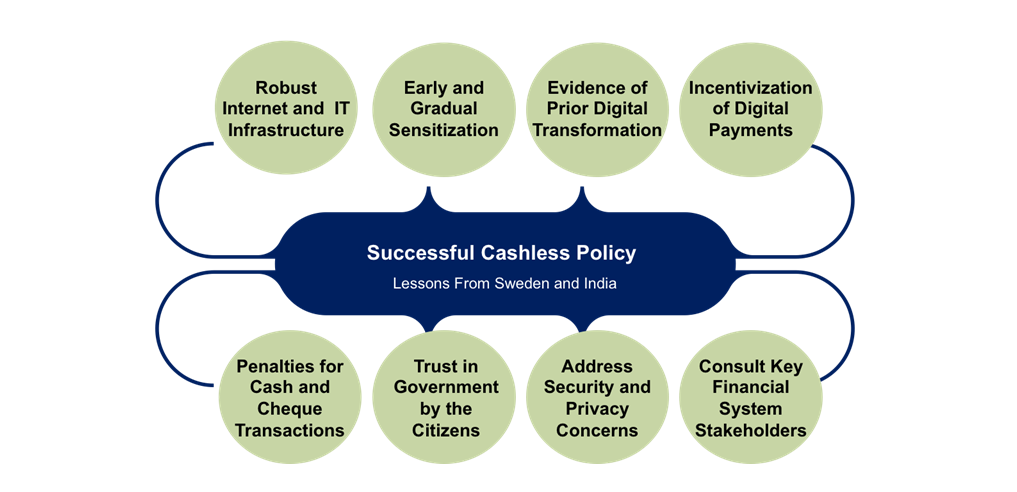

Based on the points discussed thus far, let us examine some conditions necessary for a cashless policy to be successful:

One thing is clear. When adopting a cashless policy (or any other policy for that matter), it is more important to have a customer-centric approach rather than a technical one. The success of a cashless policy is directly linked to the incentives offered to encourage mainstream adoption.

For example, the Swedish government made sure that the cost of transacting with cash was more than the cost of making card payments. There is also a trust factor that needs to be considered when it comes to convincing people to go completely digital. Additionally, a key question needs to be asked: “can our current IT infrastructure handle the increase in transaction volumes if a significant chunk of the population moves towards digital payments?”. If the answer is yes, then half of the anticipated problems are gone already.

If the answer is no, then perhaps more efforts must be made to prepare a country with a large population like Nigeria to adopt a cashless policy. According to data released by the Nigeria Inter-Bank Settlement System (NIBSS), payments made via electronic channels hit an all-time high value of N42 trillion in December 2022.

This is a 52% year-on-year increase from December 2021. Similarly, the total volume of transactions processed by NIBSS also jumped from N3.4 billion in 2021 to N5.1 billion in 2022.

This represents a 50% increase year-on-year. This upward trend will not slow down anytime soon – does Nigeria have the right internet and IT infrastructure to handle the hyper surge in transaction volumes? Only time can tell.

The level of financial inclusion is a key factor to consider when pursuing a cashless strategy. The Guardian Newspaper tells us that Nigeria is one of the top three unbanked countries in the world, with 40% of its population without a bank account and out of the 59 million unbanked adults, 73% do not have the requisite documents to open a tier-three bank account. Furthermore, the unbanked population are characterised by low levels of education, extreme poverty and are usually concentrated in rural areas.

For instance, Kaduna is arguably the most modernised state in the north; yet, up to two local governments are still without bank branches.

In addition, POS machines are also ineffective due to a lack of a strong network in these areas, and residents would need to travel at least 200 kilometres to the nearest bank branch to deposit old notes, without knowing when to expect the new notes!

The cashless situation has led to ATM vandalism, the burning of banks, the threatening of bankers and violent protests across the entire country. As turmoil spreads across the nation, it has laid bare one inescapable fact – that the poor and disadvantaged are bearing the brunt of the collapsing economy.

There is a glimmer of hope, however, that the cashless strategy is not without its benefits to the Nigerian economy. For instance, a recent report by TechPoint Africa revealed that CBN could not account for N26.17 trillion in 2021.

In contrast, N1.9 trillion of unbanked currency has since been recovered and accounted for since the launch of the new naira notes. The CBN governor, Godwin Emefiele said that as of October 2022, more than 80% of the N3.2 trillion ($7.2 billion) in circulation in Nigeria was held privately, but 75% of that has now been deposited with financial institutions.

The cashless strategy, therefore, serves as a tool to control inflation, increase transparency and financial system stability which is the key mandate of the apex bank. Secondly, the timing of the policy around the upcoming presidential elections could make vote buying and bribes more difficult than ever before.

Finally, could this be the push we so desperately needed to achieve the goals of the National Financial Inclusion Strategy (NFIS) of 95% inclusion by 2025? In particular, the Shared Agent Network Expansion Facility (SANEF) initiative of the CBN and Bankers Committee must be commended for bringing financial access to remote areas and increasing the number of agents from just over 38,400 in December 2018, to 1.4 million agents in October 2022. It presents the possibility of a world where people living in remote areas would not need to travel long distances to carry out banking activities.

The rise of financial technology (FinTech) companies in Nigeria has revolutionised the way we perceive and consume financial services. Nigeria is now the third African country with the most progress in FinTech activity, following South Africa and Kenya.

Digitally-led banks and FinTechs with strong e-payment capabilities are leveraging the cashless strategy to drive further growth and focus on operational efficiency. The witnessed jump in transaction volumes will serve as a strong foundation to build more value-added services for different classes of consumers.

If done properly, FinTechs could win over the portion of the populace that was once sceptical about their services. Additionally, many banks are establishing standalone payment services to drive the efficacy of online transactions. As Nigeria transitions into a cashless economy, great prospects lie ahead for payment service providers in terms of a larger consumer base, a wider range of services offered and ultimately, revenue growth.

We are eager to hear your thoughts on this riveting subject. Is the drive for a cashless economy by CBN a strategic or a suicidal move?

How can FinTechs create viable and profitable solutions to address the situation? Drop a comment below to keep the conversation going!

God bless Nigeria.

Thought Leadership by FintechNGR