Carrots and tomatoes are sold in modern retail outlets, yet most consumers choose to buy groceries from informal channels and traditional stores, writes Nelly Nneli

This is not a function of income levels but rather a testament that informal retailing is a vital part of Africa’s economy.

Furthermore, according to Quartz, 85.5% of Africans are engaged in the informal sector, which, according to statistics provided by the International Labour Organization, produces about 55% of their overall GDP.

Despite carrying so much significance, from street hawkers to open-market kiosks, these unregistered or unlicensed retailers—as Euromonitor puts it—transact business in vulnerable conditions, with limited access to modern financial services (UNU-WIDER, 2021) and are therefore cash-reliant. Consequently, their operations are difficult to monitor, track, or tax by government authorities.

The informal sector felt no use for modern financial services until the pandemic.

The Catalyst Effect of COVID-19 on Fintech Adoption

Indeed, COVID-19 put the traditional ways of doing business in total disarray. When sudden yet crucial survival measures, including worldwide lockdowns and social distancing, were taken, it disrupted business transactions and many trades ground to a halt.

Operations became particularly daunting for informal retailers amidst worsened cashflow issues, difficulty in inventory restocking, and lack of access to loans.

However, the outbreak of the COVID-19 pandemic aided digital transformation across the continent—a blessing in disguise.

Although it brought huge challenges, it fostered an environment where fintech services have become critical in reshaping and supporting this vital sector. For instance, research conducted by UNU-WIDER in 2021 shows that the productivity of informal retailers who use digital technology is about 65%—77% higher than that of those who don’t.

Fintech emerged as a saviour, with digital platforms like e-payments and inventory management tools that sought to boost businesses’ continuous transactions regardless of time, place, or physical presence.

These innovations are alternatives to business-as-usual, which informal retailers became compelled to explore for survival.

Since recovery from the pandemic, fintech has provided several solutions that have shaped the African economic landscape as detailed below:

1. Mobile Banking:

Shifting from cash transactions to digital payments has given informal retailers the breakthrough that they had long desired.

The likes of Paga, EcoCash and MTN Mobile Money have built platforms that drastically reduce their reliance on cash payments, which not only secure their finances but further enhance the efficiency of their business operations.

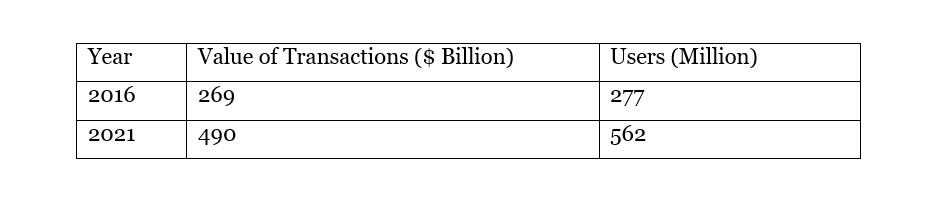

A report by GSMA evidences the embrace of this fintech innovation, revealing that in 2020, mobile money transfers in Sub-Saharan Africa rose by 23%, amounting to $490 billion.

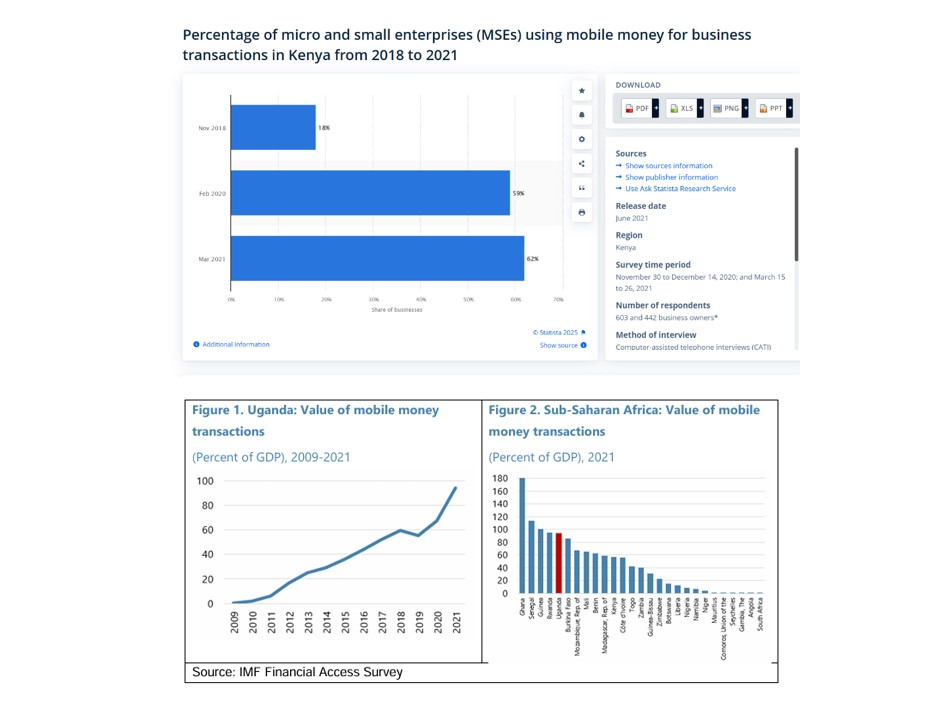

In Kenya alone, 60% of informal retailers used mobile money in 2021, according to Statista, while the same innovation accounted for 94% of Uganda’s GDP in the same year, as recorded by the IMF.

With more informal retailers subscribing to these platforms, the government can also better monitor informal transactions and levy taxes accordingly.

2. Microfinancing Platforms:

Informal retailers struggled to access loans due to their lack of proper financial records. However, with alternative data, fintech companies like M-Pesa, Branch, and Carbon can assess their creditworthiness and offer them microloans. A report by The Saturday Standard highlights that Kenya’s digital lending market grew by 13% from 2020 to 2021. The ability of informal retailers to access credit digitally has, therefore, proven invaluable, spurring all-around economic growth across the continent.

3. Inventory Management Tools:

Fintech firms have provided working solutions to informal retailers’ improper ways of managing inventory. The likes of OmniRetail, Zoho Inventory and Wasoko enable retailers to track orders, manage products and balance stock levels through software applications.

Chari’s inventory app–Karny–even allows store owners to track debts, issuing out reminders to defaulting customers. This innovation is making a remarkable impact on informal retailers.

McKinsey’s finding that digitizing supply chains could reduce inventory costs for retailers by 20%- 50% corroborates the potential of these tools to improve profitability.

4. Digital Marketplaces:

With digital marketplaces like Jumia, informal retailers can sell their products online. This ensures that the company can reach a wider customer base and diversify its income streams, which is crucial in the post-COVID era.

5. Financial Literacy Tools:

To help informal retailers understand and utilize digital financial tools, fintech companies like Pezesha and FinAccess provide training on budgeting, saving, and investing, fostering long-term financial health.

Intensifying Fintech’s Penetration of the African Informal Retail Market

Fintech solutions are undoubtedly refining the African informal retail sector; however, some challenges hinder it from reaching its full potential.

Challenges:

- Limited Digital Infrastructure: Although access to the internet and smartphone devices across Africa is improving, it is still largely inconsistent. Statista records that smartphone penetration in Sub-Saharan Africa in 2021 stands at 48%, leaving a significant portion of the population without access to fintech tools.

- Trust and Literacy Issues: Many informal retailers have limited financial literacy, and their fear of fraud makes them reluctant to adopt digital tools. It is, therefore, vital that fintech builds trust through education and reliable customer support.

- Regulatory Barriers: Africa’s fintech regulatory space is still developing. The government and regulators have yet to strike a balance between ensuring compliance and fostering innovation.

Opportunities

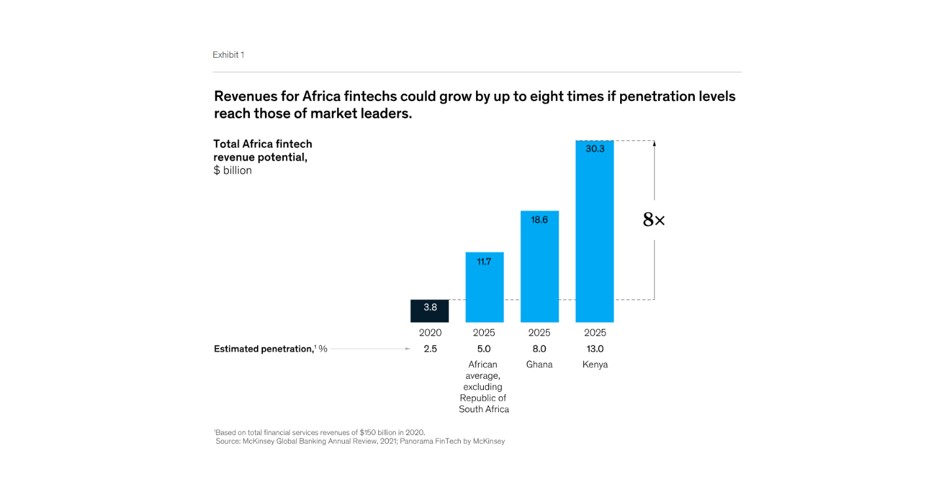

While challenges abound, the opportunities for fintech in Africa are expansive. As McKinsey projects, the African fintech market will grow at a compound annual rate (CAGR) of 10%, reaching $230 billion by 2025.

This growth opportunity shows that fintech solutions that are even more tailored to informal retailers’ unique needs will likely emerge. Technology such as AI, machine learning, blockchain, and Buy Now, Pay Later (BNPL) models have the potential to expand credit access and enhance supply chain visibility to previously underserved retailers.

In conclusion, the post-COVID era underscores the importance of resilience and adaptability, and by addressing their critical pain points, fintech has offered Africa’s informal retail sector a path to survive and thrive. With the government’s recognition of the transformative power of fintech and adequate investment in it, Africa can build a resilient economy on a global stage.

About the Author:

Nelly Nneli is a digital sales leader with a focus on making financial inclusion innovations accessible and actionable. With expertise in payment technologies and a passion for fostering inclusive finance, Nelly regularly shares her insights on the intersection of technology and financial services, offering clear, practical strategies for driving digital innovation and expanding access to financial solutions.