Fintech experts at Tipalti share their insights on the unbanked population rates in America and how fintech innovations contribute to improving financial inclusion.

Unbanked rate by demographics

In 2022, 6% of adults were ‘unbanked,’ meaning that they do not have access to traditional banking services, such as savings or checking accounts.

Those without bank accounts often rely on more expensive and less secure alternative financial services like check cashing and payday loans. This remains unchanged from 2021.

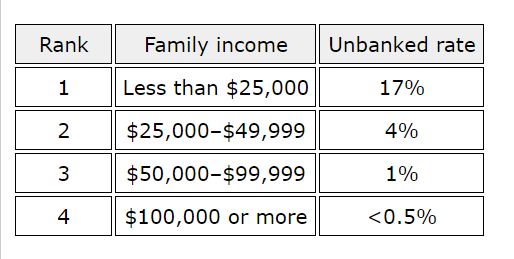

Unbanked rate by family income

Research suggests that unbanked rates are particularly high among adults from low-income backgrounds. Last year, up to 17% of adults with an annual income of less than $25,000 were unbanked.

This is significantly higher when compared to the 1% of adults with an income of between $50,000 and $99,999.

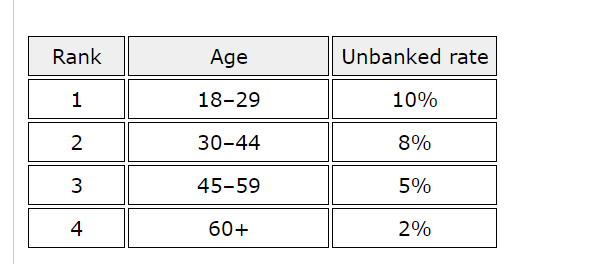

Unbanked rate by age

Young adults have the highest unbanked rate, with 10% of people within this age group lacking access to traditional banking services. 8% of individuals aged 30 to 44 also have a relatively high unbanked rate, while those aged 60+ have the highest level of bank account ownership.

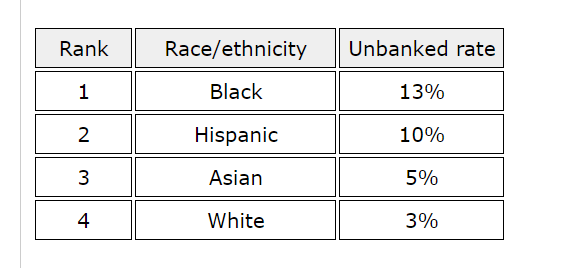

Unbanked rate by race

In 2022, unbanked rates were higher among Black (13%) and Hispanic (10%) adults. Interestingly, although traditional payment and credit methods were lower among these ethnicities, they tended to use relatively new financial services more, such as cryptocurrency for transactions and Buy Now, Pay Later (BNPL).

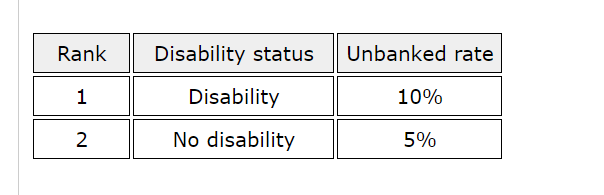

Unbanked rate by disability status

Regarding disability status, unbanked rates tended to be higher among those with a disability. In fact, adults with disabilities (10%) are twice as likely not to have access to traditional banking services compared to adults without a disability (5%).

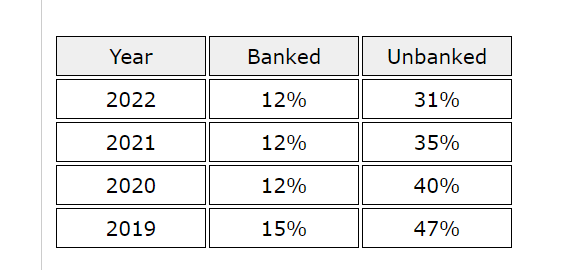

Nonbank check cashing and money orders

According to statistics, 12% of adults used nonbank check cashing or money orders in 2022. Though this remains unchanged in the last couple of years, there has been a 3% decrease from 2019.

Despite both banked and unbanked adults using nonbank providers to conduct financial transactions, there was a much higher rate among unbanked adults.

While only 12% of banked adults used a nonbank money order or check cashing service, 31% of unbanked adults also did the same. The use of nonbank money orders and check cashing has fallen by 16% among unbanked adults since 2019.

Finance operations experts at Tipalti have provided valuable insight on how fintech innovations can contribute to improving financial inclusion:

“Fintech innovations are a game-changer for financial inclusion in America. Traditional banking can be inaccessible and costly for many people, particularly people from minority groups.

While access to banks is often limited for people in remote or underserved areas, we do know that 85% of Americans use smartphones. By stepping in to fill the gap, fintech companies within the industry offer digital banking solutions that are convenient, affordable, and user-friendly. For example, mobile banking apps and digital wallets enable people from different backgrounds to access basic banking services using their smartphones – eliminating the need for physical banks.

Most importantly, the development of fintech banking platforms is redefining lending practices as they use alternative data sources and innovative algorithms to assess creditworthiness, allowing individuals with limited credit histories to access loans and credit on fair terms. This is a crucial step in reducing the reliance on predatory lending options such as payday loans.

In summary, fintech innovations are reshaping the financial landscape both in the United States and globally, making it more inclusive and accessible to all. By leveraging technology, these innovations can help decrease unbanked rates and empower individuals and communities to manage their finances better while also improving their financial well-being”

Using data from the Economic Well-Being of U.S. Households in 2022, the researchers analyzed the Banking and Credit section statistics, particularly looking at bank account ownership, the unbanked rates among different demographic groups, and the use of nonbank check cashing and money orders among banked and unbanked adults.

[Featured Image Credit]