Africa’s financial sector is undergoing a major shift, driven by technology, changing regulations, and growing consumer needs.

With the world’s youngest population and a digital economy expected to hit $180 billion by 2025, the continent is set for a financial revolution.

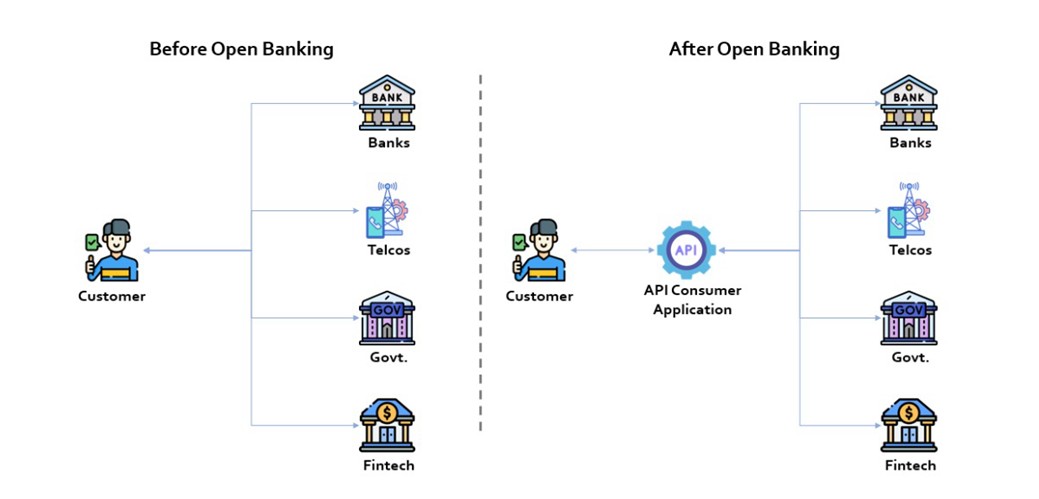

Open banking APIs are at the center of this change, allowing secure data sharing between banks and third-party providers.

Nigeria is leading the way, with other countries catching up, promising more accessible, efficient, and innovative financial services across Africa.

Understanding Open Banking APIs

Open banking is a modern financial services model that allows third-party providers like fintechs, startups, and other innovators to access consumer banking data, transaction histories, and financial services from banks and non-bank institutions via Application Programming Interfaces (APIs).

These APIs serve as secure bridges, facilitating communication between disparate financial systems and unlocking a wealth of opportunities for innovation.

Open banking represents a seismic shift in Africa, where financial ecosystems are diverse, ranging from traditional banks to mobile money platforms and informal savings groups.

Unlike the historically closed banking models that dominate many regions, open banking promotes secure data sharing (with customer consent), addressing long-standing challenges like financial exclusion, fragmented infrastructure, and limited interoperability.

From Nigeria’s bustling fintech hubs to Kenya’s mobile money dominance, this framework is paving the way for a more connected and inclusive digital economy..

The Current State of Open Banking in Africa

Africa’s journey toward open banking is uneven but promising, with 11 countries having initiated frameworks or pilots. The continent’s digital payments market is expected to hit $40 billion by year-end, and open banking APIs are accelerating this growth.

Yet, adoption remains low, hovering at 3-5% of banking customers continent-wide due to infrastructure gaps, regulatory disparities, and limited awareness. Below is a snapshot of the state of play in key markets:

Nigeria (West Africa)

Nigeria, Africa’s largest economy, is a trailblazer in open banking. In 2021, the Central Bank of Nigeria (CBN) introduced its Regulatory Framework for Open Banking, one of the continent’s first.

By 2024, the Nigeria Inter-Bank Settlement System (NIBSS) will have advanced technical standards, with 18 banks and 30 fintechs rolling out API capabilities.

Adoption stands at 6% of banking customers, up from 5% in 2024, but challenges like awareness and infrastructure persist. Nigeria’s progress positions it as a model for others.

Kenya (East Africa)

Kenya lacks formal open banking regulation, but its mobile money ecosystem, led by Safaricom’s M-Pesa, has driven organic API adoption.

M-Pesa’s Daraja API, launched in 2012, processes over $300 billion annually, with ~10% of its 51 million users engaging with third-party services like lending apps.

The absence of a regulatory framework, however, limits broader banking integration.

South Africa (Southern Africa)

South Africa’s Financial Sector Conduct Authority (FSCA) is finalizing an open finance position paper for mid-2025. Major banks like Standard Bank have piloted APIs since 2023, with adoption at ~7% of banking customers.

The country’s mature banking sector contrasts with high compliance costs and legacy system challenges.

Egypt (North Africa)

Egypt’s Central Bank introduced open banking guidelines in 2023, focusing on fintech integration. Fawry, a payment giant, leads with APIs serving 39 million monthly users.

Penetration is at ~4%, concentrated in urban areas, with rural access and trust as key hurdles.

Ghana (West Africa)

The Bank of Ghana is developing an open banking sandbox, while MTN Mobile Money drives API use. Adoption is at ~6% of mobile money users, bolstered by platforms like Zeepay, though regulatory clarity lags.

The Unique Opportunity for Africa

Open banking’s potential in Africa is profound, amplified by the continent’s unique challenges and opportunities:

1. Financial Inclusion Challenges

According to the World Bank, approximately 350 million adults in Sub-Saharan Africa remain unbanked, including 75 million in Nigeria alone.

Mobile money, used by 600 million Africans, offers a foundation, but open banking APIs can take this further by:

- Enabling accessible financial products for underserved segments.

- Reducing costs through competition and efficiency.

- Supporting alternative credit scoring using mobile and transaction data.

- Integrating informal financial systems (e.g., Kenya’s chamas) into formal channels.

2. Fragmented Financial Infrastructure

Africa’s 54 countries host a patchwork of financial systems, Egypt’s card-based networks, Nigeria’s bank-fintech hybrids, and East Africa’s mobile money dominance. Open banking APIs can unify these silos by:

- Creating seamless customer experiences across providers.

- Lowering integration costs with standardized interfaces.

- Enhancing interoperability between banks, mobile money, and fintechs.

- Strengthening system resilience, as seen in pilots by the West African Economic and Monetary Union (WAEMU).

Early Market Impact and Success Stories

Open banking APIs are already driving tangible change across Africa’s financial landscape, even in their nascent stages.

From fintechs enhancing credit access to mobile money platforms powering commerce, early adopters leverage APIs to innovate, improve financial inclusion, and boost efficiency.

Below are standout examples from key markets, illustrating the diversity and potential of open banking across the continent.

Nigeria: Carbon and Okra

In Nigeria, open banking is fueling a fintech revolution. Carbon has harnessed banking APIs to refine its lending platform, disbursing over ₦57 billion (~$40 million) to 2.5 million customers by 2024.

PalmPay, Carbon Join Forces with Verve to Give Over 30 million Customers Access to Verve cards

By securely accessing customer banking data (with consent), Carbon has built sophisticated credit-scoring models that reduced loan default rates by 38% compared to traditional methods.

The platform reports a 15% uptick in loan disbursements year-over-year, reflecting growing trust in API-driven services.

Meanwhile, Okra has emerged as a “super-connector,” linking over 200 businesses to bank accounts via its API platform and processing over 350 million API calls.

Okra powers use cases from lending to personal finance management, cementing Nigeria’s role as a fintech pacesetter.

Kenya: Safaricom’s M-Pesa

Kenya’s mobile money giant, Safaricom, exemplifies organic open banking through its M-Pesa Daraja API. Launched in 2012, this API enables developers to integrate payment and lending solutions, serving M-Pesa’s 51 million users across East Africa.

In 2024 alone, it facilitated $1.2 billion in microloans via third-party apps, with transaction volumes exceeding $300 billion annually.

By March 2025, ~10% of M-Pesa users (5.1 million) actively engage with API-enabled services such as KCB M-Pesa’s savings accounts or Branch’s instant loans, demonstrating how open APIs extend financial access beyond payments into credit and investment.

This ecosystem has also spurred over 1,000 local developers to build apps, fostering a vibrant innovation hub.

South Africa: Yoco and Standard Bank

South Africa’s mature banking sector is seeing open banking reshape SME finance. Yoco, a payment platform, leverages APIs to enable 150,000 small businesses to accept digital payments, processing $500 million annually.

Yoco’s API integrations with banks like FNB have cut transaction costs by 12% for merchants, boosting digital adoption in retail and hospitality.

Simultaneously, Standard Bank, a pioneer in open banking pilots since 2023, has rolled out APIs for account aggregation and payment initiation.

Serving 2 million customers with these services, Standard Bank reports a 20% increase in digital transaction volumes, showcasing how legacy banks can compete in an API-driven world.

Egypt: Fawry

Fawry dominates Egypt’s payment landscape in North Africa with its open APIs, connecting 4 million daily users to bill payments, merchant services, and mobile top-ups.

Fawry Partners Infobip to Enhance Electronic Payment Services

Fawry’s API ecosystem supports over 1,500 businesses, processing $2 billion in transactions annually and reducing cash reliance in urban centers like Cairo and Alexandria.

A standout use case is its integration with e-commerce platforms, enabling seamless checkouts that have grown online sales by 25% for partnered merchants. Fawry’s success highlights how open banking can bridge traditional and digital finance in a region with low rural connectivity.

Ghana: Zeepay and MTN Mobile Money

Ghana’s mobile money sector is a hotbed for open banking innovation. Zeepay, a remittance platform, uses APIs to streamline cross-border payments, processing $300 million in transfers in 2024. Its APIs cut remittance costs by 20%, benefiting Ghana’s diaspora community, which sent $4.5 billion home in 2024.

Ghana’s Zeepay Gets Additional $10 Million Debt Funding From Verdant Capital

Meanwhile, MTN Mobile Money’s APIs power bulk disbursements and merchant payments, serving 23 million users.

By the end of 2024, MTN reports 1.5 million API-driven transactions monthly, including payroll for SMEs, illustrating how open banking enhances operational efficiency.

Rwanda: Irembo

Rwanda’s Irembo platform showcases open banking’s public sector potential. Launched as a government e-services portal, Irembo integrates banking APIs to link citizen accounts with taxes, licenses, and utilities payments. It currently serves 3 million users and processes $150 million in transactions annually.

A key success is its partnership with the Bank of Kigali, which enables real-time tax reconciliation, cutting processing times for small businesses by 60%.

Irembo’s model demonstrates how open banking can simultaneously modernize governance and financial inclusion.

Morocco: Attijariwafa Bank

In North Africa, Attijariwafa Bank leverages APIs to bolster trade finance for SMEs. its open banking platform supports $100 million in export financing annually, up 30% from 2024.

APIs integrate transaction data with supply chain insights, enabling faster loan approvals, often within 24 hours, compared to weeks under traditional systems.

This has empowered 5,000 Moroccan exporters, particularly in agriculture and textiles, to compete globally, showing how open banking can drive economic diversification.

Uganda: Beyonic

In East Africa, Uganda’s Beyonic uses APIs to streamline bulk payments for businesses and NGOs. Beyonic processes $80 million annually across 500 organizations, including disbursements to rural farmers and aid recipients.

Its API integrations with MTN Uganda and Airtel Money cut transaction fees by 15% and delivery times by 50%, enhancing financial access in a country where 40% of adults remain unbanked.

Impact Snapshot

Collectively, these early successes underscore open banking’s versatility, spanning lending (Nigeria, Kenya), SME finance (South Africa, Morocco), remittances (Ghana), public services (Rwanda), payments (Egypt), and disbursements (Uganda).

API-driven services have reached over 30 million Africans, with transaction values exceeding $305 billion annually across these examples alone.

While adoption varies, highest in Kenya (10%) and lowest in Egypt (4%), the momentum signals a broader shift toward an API-first financial ecosystem.

Challenges and Barriers to Fully Implementing Open Banking in Africa

While open banking holds immense promise for transforming Africa’s financial landscape, its implementation faces formidable obstacles.

These challenges span technological, regulatory, social, and economic dimensions, reflecting the continent’s diverse and complex environment. Addressing them is critical to unlocking the full potential of open banking and ensuring it delivers inclusive, efficient financial services.

Below are some of the key barriers:

1. Data Privacy and Security Concerns

The pervasive lack of trust in data-sharing systems is a fundamental barrier to open banking adoption. Many Africans hesitate to share financial data with third parties, a concern amplified by high-profile security breaches.

In Nigeria, sensitive government-held information was sold for as low as 100 naira on some unauthorized websites in 2024, while South Africa saw a 2024 cyberattack compromise 1.2 million accounts.

Across Sub-Saharan Africa, cybercrime costs businesses $4.5 billion annually (Interpol, 2023), with financial institutions bearing a significant share.

2. Technical Infrastructure Challenges

Africa’s digital infrastructure remains a critical bottleneck. Internet penetration across the continent stands at 43% as of 2024, up from 36% in 2023 but well below the global average of 67%.

Rural areas, home to 60% of Africa’s 1.4 billion people, suffer the most from mobile network coverage, which is often limited to 3G. Power outages further complicate connectivity; Nigeria, for example, averages 206 hours of blackouts monthly.

For banks and fintechs, maintaining seamless API-driven systems under these conditions is daunting. Legacy banking systems compound the issue; in 2024, five central Nigerian banks (Access, Zenith, UBA, GTBank, and Wema) spent ₦178.77 billion ($105 million) on IT upgrades, a 203% increase from 2023, yet many still rely on outdated infrastructure ill-suited for open banking. Scaling APIs across such uneven terrain requires a massive investment.

3. Regulatory Challenges and Uncertainty

Africa’s open banking landscape is fragmented, making cross-border adoption difficult. While Nigeria set a strong precedent with its 2021 framework, only 11 out of 54 African countries have similar regulations or a pilot program.

Despite M-Pesa’s success, Kenya lacks formal open banking rules, while South Africa plans to introduce its open finance guidelines by mid-2025. Ghana’s regulatory sandbox, expected in late 2025, highlights the slow pace of adoption elsewhere.

This lack of uniformity creates uncertainty; fintechs and banks hesitate to invest without clear regulations. Scaling across Africa is also tough due to differing KYC requirements and data standards in the 54 markets under the African Continental Free Trade Area (AfCFTA).

Though efforts like the Open Finance African Group’s regional API standards aim to address these gaps, progress remains slow due to limited funding and coordination.

4. Low Digital and Financial Literacy

Limited digital and financial literacy undermines open banking’s reach. In Sub-Saharan Africa, financial literacy averages 32%, far below the 52% in high-income countries.

A 2024 World Bank survey found that 45% of unbanked adults in the region cite a lack of understanding as a barrier to account ownership, with rural women disproportionately affected.

In Egypt, only 27% of adults are financially literate, while in South Africa the figure is 42%. Educating 1.4 billion people across diverse languages and cultures is a monumental task, slowing adoption.

5. Financial Exclusion and Economic Barriers

Open banking relies on financial access, but 350 million adults in Sub-Saharan Africa are still unbanked, including 75 million in Nigeria.

While mobile money is growing—49% of adults now have an account—traditional banking lags at just 29% (Global Findex, 2024).

Poverty makes this worse. Over 431 million Africans live on less than $1.90 a day, making banking fees unaffordable.

Africa’s largely informal economy adds another challenge. Many small businesses and individuals lack formal records, making integrating them into API-driven financial services difficult.

My Perspective on Open Banking in Africa: The Next Five Years

If current trends continue, open banking could drive significant changes in Africa’s financial landscape over the next five years, particularly in financial inclusion, cost reduction, economic growth, credit expansion, and API adoption.

- Expanding Financial Inclusion: Africa remains home to the largest unbanked population globally, with over 350 million adults lacking access to formal financial services. Open banking could play a transformative role in reaching these individuals, particularly in mobile-first economies like Kenya, Ghana, and Côte d’Ivoire. By enabling secure, API-driven financial products, more people can access banking, lending, and insurance services without visiting traditional banks.

- Lowering Costs for Financial Services: API standardization can significantly reduce operational costs for banks and fintech companies. Analysts estimate that this could lead to a 25–40% reduction in service costs, making financial products more affordable for consumers across Africa, where high banking fees often deter participation in formal financial systems.

- Boosting Economic Growth: As financial institutions and fintechs leverage open banking frameworks, digital transactions are expected to surge. In Nigeria, digital payments are projected to grow by 15% annually, while in South Africa, API adoption is expected to drive a $3 billion increase in fintech investments by 2027. These advancements will enhance economic growth by facilitating seamless transactions and encouraging new financial innovations.

- Expanding Access to Credit: Lenders can make more informed credit decisions with better access to consumer and business financial data. Across Africa, where small and medium enterprises (SMEs) struggle to secure loans due to a lack of credit history, open banking could increase lending opportunities by 30–50% over the next five years.

- Growth of the API Ecosystem: The adoption of open banking APIs is expected to skyrocket, particularly in countries with strong fintech ecosystems like Nigeria, South Africa, and Kenya. The number of API calls processed through open banking infrastructure is projected to grow from 1.2 billion in 2024 to over 15 billion by 2029.

The Future of Open Banking in Africa

Open banking APIs have the potential to reshape Africa’s financial landscape by enhancing financial access, fostering innovation, and increasing efficiency.

- For consumers: More personalized, affordable, and accessible financial services.

- For banks and fintechs: New revenue streams, strategic partnerships, and improved customer engagement.

- For Africa as a whole: A path toward greater financial inclusion and economic development.

However, realizing this vision requires:

- Stronger security frameworks to build public trust.

- Clearer regulatory guidelines to encourage adoption.

- Consumer awareness campaigns highlighting the benefits of open banking.

Africa has the opportunity to lead in open banking innovation, not by replicating Western models but by tailoring solutions to the continent’s unique needs.

The API-driven financial revolution is just beginning, and its impact over the next decade could be transformative, unlocking new economic opportunities across the region.

About the Writer:

Motunrayo Koyejo is a software engineer with a difference. She is passionate about improving financial technology through innovative engineering.

As a Backend Engineer, she has a knack for building reliable, high-performing systems. Motunrayo specializes in backend technologies like PHP, Laravel, Typescript, NestJS and AWS, focusing on creating solutions that scale and solve real-world problems efficiently.

She is a stronger believer in using technology to simplify complex challenges, whether it’s optimizing performance, improving security, or integrating seamless APIs.