A quiet revolution is taking root in global digital finance, and it’s not coming from banks or legacy platforms. It’s being driven by open infrastructure, and at the heart of this change is Open Payments.

As of 2023, over 350 million adults in Sub-Saharan Africa remain unbanked, even as more than 600 million people use mobile money. Yet, sending money across borders still comes with high friction and even higher costs; remittance fees average 8.2%, the highest globally.

Globally, momentum is building around Open Payments, with more than 40 financial institutions and digital wallets actively exploring or integrating the standard. Open Payments-enabled transactions are already taking place across over 60 countries, demonstrating its growing global reach.

This article dives deep into the Open Payments standard, what it means for Africa’s digital future, and how the continent’s mobile-first innovation and youth-driven tech culture make it the ideal launchpad for a more inclusive financial system.

Introduction to Open Payments

Digital payments have come a long way, but they’re still more complicated than needed, especially if you’re sending money across borders, between platforms, or without a bank account.

Today, most people rely on third-party processors like PayPal or Stripe to handle payments. These work well, but they come with strings attached: high fees, long wait times, and limited control over how money moves.

Now imagine if making a payment online was as simple and open as sending an email. No matter which provider you use or where you are in the world, you’d just need the other person’s “address” and the payment would go through instantly.

That’s the vision behind Open Payments

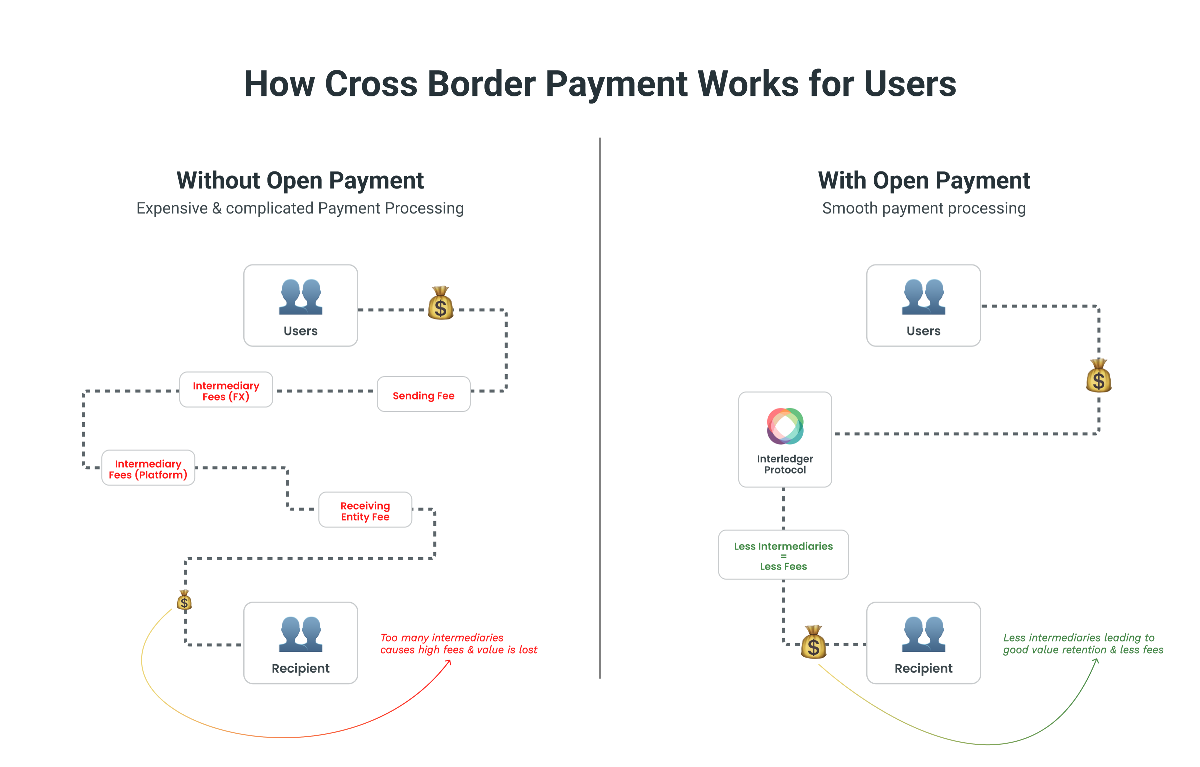

Open Payments is an open standard powered by the Interledger Protocol (ILP) that allows money to move between different financial systems, just like the internet allows information to move between websites and devices.

At the heart of Open Payments is a simple idea: You should be able to send and receive money easily, regardless of what platform you’re using.

Here’s how it works, in plain terms:

1. Payment Pointers

Open Payments replaces long, complex banking details with something simple and human-readable called a Payment Pointer. Think of it like a username or web address for receiving payments—something like: $alice.wallet.com or $yourname.africa

A Payment Pointer is not a wallet address in the crypto sense. Instead, it points to a web-accessible endpoint (usually a URL) hosted by your financial service provider or wallet. When someone wants to send you money, their system queries this endpoint to discover how to complete the payment securely using the Interledger Protocol (ILP).

2. One Connection, Many Possibilities

Without Open Payments, every app or service you want to send money from has to build a separate connection to every possible bank, wallet, or mobile money provider. That’s a nightmare.

With Open Payments, a single integration gives you access to any provider that supports the standard. No need to write hundreds of custom APIs. Just one.

3. Secure, Consent-Driven Transactions

You’re always in control. When someone wants to send or pull funds from your wallet, they have to make a request, and you decide what’s allowed. You can approve a single transaction, set limits, or even authorize recurring payments with specific rules.

Think of it like granting Netflix access to charge your card monthly, but safer, more flexible, and not tied to credit cards at all.

4. No More Middlemen (Unless Necessary)

Open Payments reduces reliance on traditional intermediaries, which usually add fees and delays. If currency conversion or settlement routing is needed, the system finds the best path automatically using Interledger. But you’re not stuck paying unnecessary layers of fees just to send $10 across borders.

5. Works for Everyone, Not Just Banks

You don’t need a traditional bank to use Open Payments. Whether you’re using a mobile wallet, a crypto app, or a community savings platform, as long as your provider supports the standard, you’re in the network.

That’s a game-changer for billions of people around the world who are underbanked or unbanked.

The Current State of Open Payments in the World and Africa

As digital payments evolve, the global financial ecosystem is slowly but surely pivoting toward open, interoperable systems, and Open Payments is at the center of that transformation.

While adoption is still in its early stages, there is growing momentum around the world as both traditional financial institutions and fintech innovators begin to embrace the Open Payments standard and the Interledger Protocol (ILP).

A Growing Global Ecosystem

Open Payments is not a product—it’s an open standard. This means any institution, app, or wallet can adopt it without licensing fees or proprietary gatekeeping. And while we’re still early in the adoption curve, some notable players and platforms have already taken the lead.

- GateHub: One of the first digital wallets to support Open Payments globally. It facilitates cross-currency transactions using ILP and offers payment pointer functionality.

- Fynbos: A wallet provider in South Africa, Europe, and North America that enables Open Payments transfers between Fynbos accounts, with future plans to connect with other networks like GateHub.

- Interledger Pay: A live implementation that lets users send and request money using wallet addresses, showcasing Open Payments’s ability to work across platforms.

- Chimoney: A Canadian Fintech company has integrated Open Payments to enable seamless wallet-to-wallet transfers via Interledger payment pointers. More than just a wallet, Chimoney allows payouts to over 120 countries, supporting a wide range of disbursement options, including bank accounts, mobile money, and gift cards. This global reach demonstrates how Open Payments can be embedded within large-scale financial systems to deliver inclusive, programmable, and borderless payouts.

These early implementations are proof of concept for what’s possible, but widespread adoption still requires deeper integration by banks, mobile money providers, and governments.

Current Metrics and Trends

- As of early 2025, over 40 financial services companies have expressed interest or are in the process of integrating Open Payments.

- Open Payments-enabled transactions have occurred in over 60 countries, primarily through test wallets and early-adopter platforms.

- Payment pointers—human-readable wallet addresses—have been issued to tens of thousands of developers through tools like the Interledger Test Wallet and GitHub starter kits.

- The Interledger Foundation has announced over $21 million in investments and strategic partnerships to expand interoperable payment solutions globally, signaling a growing institutional commitment to Open Payments and its ecosystem.

- Developer interest is surging: repositories like interledgerjs and open-payments have seen significant spikes in stars, forks, and community contributions since mid-2024.

This traction is being driven in part by the protocol’s promise of cost savings, security, and inclusivity, especially in low-income and underbanked regions.

The Situation in Africa

Africa has long been a leader in mobile-first financial innovation. Yet, despite the success of mobile money platforms, the continent still grapples with fragmented financial infrastructure, high remittance fees, and lack of interoperability across borders.

This makes Africa a prime use case for Open Payments.

- 600 million mobile money users across Sub-Saharan Africa.

- 8.2% average remittance fee to Sub-Saharan Africa.

- 350 million unbanked adults in the Sub-Saharan African Region, with most relying on informal savings groups or community wallets.

Today, even leading mobile money systems like M-Pesa, MTN Mobile Money, and Airtel Money still require closed-loop integrations. This means a user on one platform can’t always send funds to someone using another unless they pass through banks or costly intermediaries.

Open Payments offers a compelling alternative. By introducing a standardized way to send money across providers, it reduces friction, lowers costs, and boosts access.

While there are no fully live, cross-provider Open Payments deployments in Africa yet, wallets like Fynbos in South Africa and Open Payments-based projects led by African developers are laying the foundation.

The Unique Opportunity for Africa

Africa has always done things a little differently when it comes to money. While the West focused on banks and cards, Africa leapfrogged into mobile money. That’s how platforms like M-Pesa became household names and helped millions send, spend, and save without ever stepping into a bank.

But here’s the problem: most of these systems don’t talk to each other.

You can’t easily send money from your mobile wallet in Nigeria to someone’s bank account in Ghana. Even within the same country, users on different platforms often have to jump through hoops to transfer funds. It’s like trying to send an email from Gmail to Yahoo and needing five apps to do it.

That’s where Open Payments changes the game.

Why Africa is the perfect place for Open Payments

- Cross-border is our daily life

Africa is made up of 54 countries, and millions of people live, work, and trade across borders. Whether it’s traders in Cotonou sending money to Lagos or a freelancer in Nairobi getting paid from the UK, cross-border payments aren’t a “nice to have”—they’re essential. Open Payments is built exactly for that: simple, low-cost, borderless payments. - Mobile-first means we can move fast

Most Africans already use mobile wallets. With Open Payments, these wallets can be upgraded to speak the same financial language without replacing them. It’s not about building something new from scratch. It’s about connecting what we already have. - A young, tech-savvy generation

With the continent’s median age at just 19, Africa has the youngest population on Earth, and that means a lot of builders, developers, and early adopters ready to shape the next wave of fintech.

This is a generation that already uses crypto, virtual cards, social commerce, and gig platforms. Open Payments is the natural next step—a tool that matches their global mindset.

What makes Open Payments so powerful for Africa?

- No more vendor lock-in: A wallet or app that supports Open Payments can connect to any other one that does, too. Users aren’t stuck with one provider.

- Fewer fees, more control: By cutting out unnecessary middlemen, Open Payments reduces costs and gives users more transparency on who gets what.

- One wallet address, many use cases: Just like an email address, users can share a wallet address and get paid from anywhere (apps, websites, employers, family abroad).

- It works across banks, wallets, and mobile money: Open Payments isn’t tied to a single network. Whether it’s a bank in Lagos or a mobile wallet in Kigali, it all just works if it’s built on the standard.

Early Market Impact and Case Studies

Open Payments isn’t just a promising idea, it’s already being used to solve real financial problems for real people. Across Latin America, the Caribbean, Africa, and Asia, developers, startups, and even government-backed platforms are building practical tools powered by Open Payments.

Here are some of the examples of how Open Payments is changing lives, facilitating financial inclusion, and empowering and growing businesses today:

BessPay – Helping Creators Get Paid Instantly

In the Caribbean, BessPay is reshaping how digital creators earn income. Instead of waiting 30 days for payouts or losing up to 30% in platform fees, creators using BessPay are receiving earnings instantly through Open Payments and payment pointers.

The platform supports real-time micropayments, tipping, and content monetization tools that allow creators to cash out in local bank accounts, mobile money, or digital wallets. Early adopters have seen a 40% increase in revenue retention, as BessPay puts power and profit directly in the hands of its users.

Snake Nation – Decentralizing the Creator Economy

Snake Nation, a platform built for multicultural creators across Africa and Latin America, has integrated Open Payments into its VNM wallet to decentralize the creator economy. By removing intermediaries and empowering artists to receive direct payments from their fans,

Snake Nation has enabled real-time tips, paywalled content, and creator tokens—all powered by Interledger. Thousands of creators have already benefited from instant settlements across borders, and the platform continues to grow its user base with a mission to help artists thrive financially regardless of their geography.

ThitsaWorks – Bringing Digital Payments to Rural Myanmar

In Southeast Asia, ThitsaWorks has tackled financial exclusion in Myanmar by digitizing rural microfinance institutions through Open Payments and Mojaloop.

With over 2 million rural users connected, ThitsaWorks’ solution automates loan disbursements and repayments via mobile wallets and bank integrations.

The system has reduced loan processing times by over 50% and made financial services more accessible for users who had previously relied on cash transactions.

Their integration with Mojaloop also opens the door to cross-border transactions, improving financial resilience in economically vulnerable regions.

Cámara de la Gente – Cross-Border Remittances for Rural Mexico

Cámara de la Gente in rural Mexico is leveraging Open Payments to power a cross-border remittance hub for small credit unions and community banks.

By reducing dependency on traditional remittance services, which often charge fees upwards of 8%, the platform has successfully cut costs by over 20% while enabling instant account-to-account transfers.

This innovation is particularly impactful in rural towns where access to digital banking remains limited, giving families faster and more affordable ways to receive support from loved ones abroad.

CryptoSavannah – Loyalty Programs, Reimagined

In East Africa, CryptoSavannah is rethinking how loyalty rewards work. Instead of letting loyalty points sit unused, their Universal Wallet enables customers to earn, transfer, and redeem rewards across a network of partner merchants.

Built on ILP and Open Payments, the platform supports multi-format value, including fiat, crypto, and store credit.

Since the launch, participating retailers have reported a 2x increase in loyalty point redemption rates and improved customer retention, thanks to the flexibility and interoperability of their rewards system.

Mojaloop – Government-Grade Open Payments Infrastructure

Finally, Mojaloop is serving as the national-grade infrastructure layer for Open Payments in countries like Tanzania, Rwanda, and Myanmar.

Through partnerships with governments, central banks, and financial service providers, Mojaloop has facilitated billions of dollars in financial flows while enabling seamless transactions across banks, wallets, and MFIs.

Its integration of Interledger allows for cross-ledger interoperability, and its deployment has driven significant improvements in financial inclusion, particularly among unbanked and underbanked populations.

Challenges and Barriers to Fully Implementing Open Payments in Africa

As promising as Open Payments is for financial transformation, the road to its widespread adoption in Africa is filled with friction. Below are the major barriers slowing progress, each rooted in a unique blend of infrastructure gaps, regulatory complexity, and user behaviour:

1. Weak Digital Infrastructure

Many African regions, especially rural areas, lack consistent Internet access and mobile coverage. Open Payments thrives on low-latency, always-on connectivity, but with only 43% internet penetration continent-wide, real-time financial services remain out of reach for millions. Slow networks and frequent power outages make reliable access to wallets and APIs a significant challenge.

2. Regulatory Uncertainty

Open Payments operates across borders, platforms, and financial layers, but most African countries still don’t have policies that reflect this reality.

While Nigeria has introduced Open Banking regulations, the majority of other nations are either stuck in sandbox mode or still adapting legacy laws. This creates hesitation among banks, FinTechs, and wallet providers, who fear running afoul of compliance rules.

3. Trust and Data Privacy Concerns

Even when infrastructure is in place, user trust is another story. People are rightfully cautious about linking apps to their money, especially in environments where data breaches and financial scams are common.

Despite Open Payments offering explicit consent and granular control, the fear of “giving an app access to your account” remains a major psychological barrier.

4. Limited Incentives for Legacy Institutions

Large banks and incumbent financial service providers don’t always see the upside of embracing Open Payments. Many prefer to operate closed systems and charge high fees for access.

Since Open Payments prioritizes openness and interoperability, some institutions feel it threatens their business model. Without competitive pressure or regulatory nudges, adoption by these players may lag.

5. Low Awareness and Technical Literacy

The concept of Open Payments—wallet addresses, Interledger, GNAP (Grant Negotiation and Authorization Protocol) is still new to many businesses, developers, founders, and users.

Financial literacy remains low in many communities, and technical understanding among SME owners and local agents is still developing. Without grassroots education and easy-to-use tools, even the best technology won’t gain traction.

6. Persistent Financial Exclusion

As of 2023, over 350 million adults in Sub-Saharan Africa are still unbanked. While mobile money has made impressive strides, it doesn’t fully bridge the gap. Open payments require at least a digital wallet or interoperable account. For people without access to identity verification, smartphones, or formal onboarding channels, this is a non-starter. The foundation for access must be laid before innovation can scale.

My Perspective on Open Payments

Over the past year, my journey with Open Payments has led me to several realizations that shape not only how I view financial infrastructure but how I believe we should build it. Here’s my perspective distilled into key insights:

1. Open Payments is not just a technology—it’s a mindset shift

This is a departure from proprietary rails and fragmented systems. It’s about reimagining financial infrastructure as open, interoperable, programmable, and inclusive—the way email revolutionized communication.

2. It empowers both users and developers

With Open Payments, users control who can access their accounts, what they can do, and for how long, without exposing sensitive information. At the same time, developers no longer need to build complex, one-off integrations. One protocol, one standard, many use cases.

3. It lowers the barrier for innovation

Startups, NGOs, and indie developers can now build payment-enabled apps without becoming licensed financial service providers. This radically changes who can build in the financial space and what they can build.

4. It’s already real, and it’s already working

Throughout my 30 Days of Open Payments series, I showcased real-world case studies, wallets using payment pointers, apps using Interledger, and communities benefitting from reduced transaction friction. This isn’t hype; it’s already happening.

5. Education is key to adoption

In my session titled “Open Payments Made Simple—No-Code Solutions and Open-Source Innovations,” presented physically at Microsoft Reactor DevConnect 2025, I introduced over 100 participants, including open source enthusiasts, non-technical professionals, and developers, to the power and simplicity of Open Payments. The session demonstrated how anyone, regardless of technical background, could begin building financial tools using open standards and no-code platforms. Once people realized how accessible the technology is, a wave of interest and experimentation followed, proving that demystifying the protocol is the first step to widespread adoption.

6. Africa is poised to lead this revolution

We’ve already leapfrogged outdated infrastructure with mobile money and digital wallets. Open Payments gives us the chance to leapfrog again into borderless, low-cost, accessible financial ecosystems.

7. My mission is to bridge knowledge and action

Through my workshops, articles, and daily content, I aim to translate complex standards into usable ideas for businesses, developers, founders, and policymakers. My goal is to make Open Payments not just understandable but actionable.

The Future of Open Payments

The world of payments is shifting, and Open Payments is at the heart of this transformation. In the next five years, we won’t just talk about interoperability and financial inclusion; we’ll live it.

Imagine a future where sending money from Lagos to Lima is as easy as sending a tweet. Where a teenager in Nairobi can get paid instantly for designing a logo for a startup in Berlin. Where a nonprofit in Accra receives donations from supporters in Tokyo without paying 12% in fees to legacy platforms. This is not just possible—it’s inevitable.

Open Payments is laying the foundation for a wallet-to-wallet world. A world where financial applications speak a universal language, where developers build once and scale globally, and where people—not institutions—control the flow of their money.

We’re moving toward a future where:

- Wallet addresses become your global financial identity, recognized across apps, platforms, and borders.

- Microtransactions flourish, powering new economies from creators getting paid per view to learners tipping educators.

- Developers build plug-and-play financial apps without needing banking licenses or backend acrobatics.

- Startups from underserved regions compete on equal footing with Silicon Valley, thanks to infrastructure that no longer discriminates based on geography.

- Consent, transparency, and security aren’t features—they’re defaults. Users decide who can access their money, when, and how much.

But here’s the most exciting part: Africa isn’t catching up; we’re positioned to lead. Our mobile-first ecosystems, youth-driven innovation, and demand for financial alternatives make the continent a natural breeding ground for Open Paymentss breakthroughs. What M-Pesa was to mobile money, Open Payments could be to the next generation of financial technology across the continent.

This isn’t a distant dream. We’re building it now. From Interledger-enabled wallets in South Africa to developer workshops in Nigeria to early-stage adoption in Ghana, the ecosystem is growing. Standards are maturing. Communities are forming. Builders are shipping.

The rails of global finance are being rewritten, and Open Payments is the ink. So whether you’re a policymaker, product manager, backend engineer, or founder, the invitation is open. Open to build. Open to innovation. Open to include.

The question is no longer if Open Payments will shape the future—it’s who will shape Open Payments.

And if you ask me, it should be us.

About the Author

Babatunde Hammed is a seasoned professional with a rich blend of expertise in operations, project management, business development, and compliance. With a proven track record of optimizing business processes and delivering strategic growth, he has made significant contributions to global organizations, particularly in the fintech and Open Payments space.

As the Head of Operations at Chimoney, Babatunde plays a pivotal role in transforming the way people send, receive, and manage money across borders. He leads cross-functional initiatives focused on enabling financial inclusion, ensuring compliance with global regulatory frameworks, and scaling secure payment infrastructure. His work sits at the powerful intersection of finance, technology, and policy.

Beyond his operational leadership, Babatunde is a passionate advocate for Open Payments. He is deeply committed to educating developers, non-technical professionals, founders, and policymakers on the transformative potential of open financial systems.