African countries have been encouraged to seek alternative funding schemes to tackle climate change impacts whose effects have been exacerbated by the Covid-19 pandemic, the Russian-Ukrainian war, geopolitical fragmentation, and external shocks around the world.

According to the International Monetary Fund (IMF), the investment required for adaptation in developing countries could range from USD 50 billion to USD 500 billion annually by 2050.

The alternative funding will help Africa bolster its efforts for this course which currently depends only on Resilience and Sustainability Facility (RSF) from IMF which was initiated in 2022.

Large climate financing needs

The Covid-19 pandemic, the Russian-Ukrainian war, geopolitical fragmentation, and external shocks around the world have exacerbated the effects of climate change in developing countries, low-income countries, and Small Island and Developing States (SIDS), increasing the huge financing needs they already had.

For example, Africa will need around USD 133 billion annually in clean energy investments to meet its energy and climate goals between 2026 and 2030, according to the Climate Policy Initiative.

According to the International Monetary Fund (IMF), the investment required for adaptation in developing countries could range from USD 50 billion to USD 500 billion annually by 2050.

African countries, which make up most developing countries, would face adaptation and mitigation costs of 50 billion dollars per year by 2050.

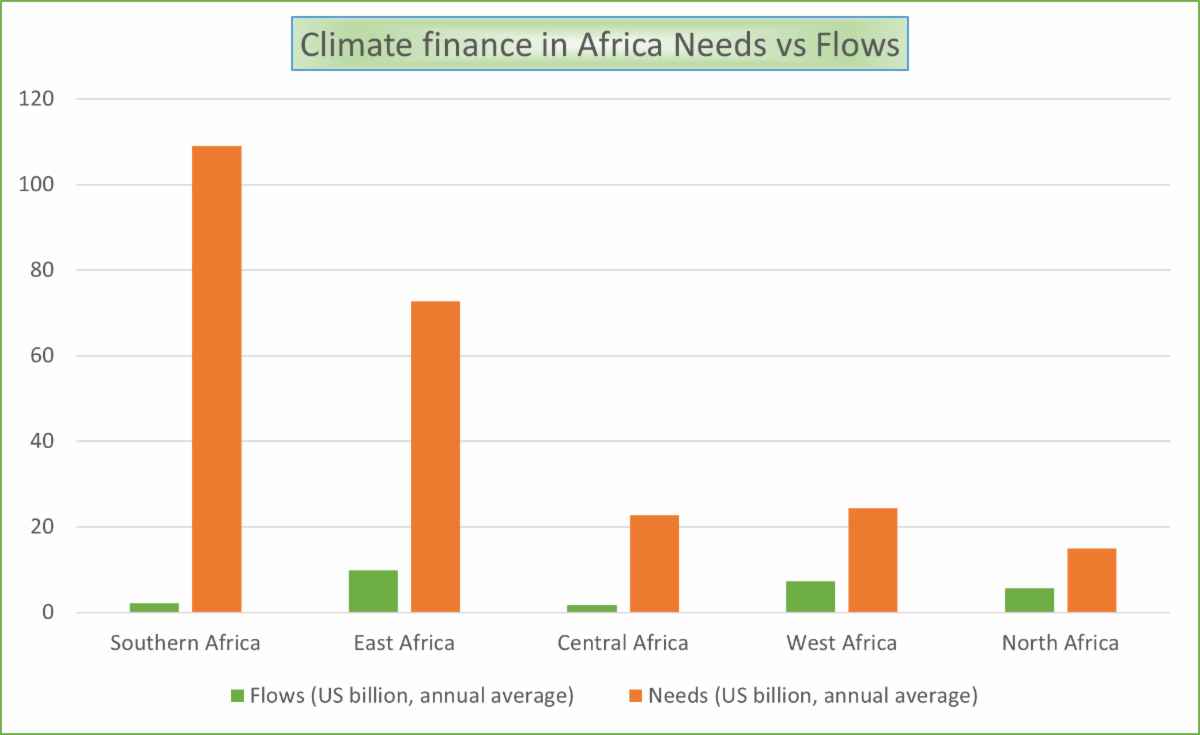

Investment deficits vary from country to country. All sub-regions receive far less funding than they need. However, the Southern African region has the largest funding gap.

This is mainly due to the high climate finance needs identified by South Africa alone ($107 billion per year), combined with one of the lowest regional levels of climate

investment. Central and East African countries have the largest climate investment gaps as a percentage of GDP: 26% and 23% on average, respectively.

North African countries have the lowest climate investment gaps (3% of GDP), but the need for climate finance in these countries still exceeds flows by three to six times.

IMF response

As part of efforts to support vulnerable countries, in April 2022 the Executive Board of the International Monetary Fund approved the creation of the Resilience and Sustainability Facility (RSF), which is financed by voluntary contributions from IMF members with a strong external position, including through the reallocation of surplus Special Drawing Rights (SDRs).

The IMF set up this new financing instrument to help low- and middle-income countries and Small Island Developing States meet the challenges of adapting to climate change and pandemics.

To date, the only African countries to benefit from IMF loans under the RST are Rwanda, Senegal, and Seychelles for amounts of USD 310 million, USD 327.1 million, and USD 46 million respectively.

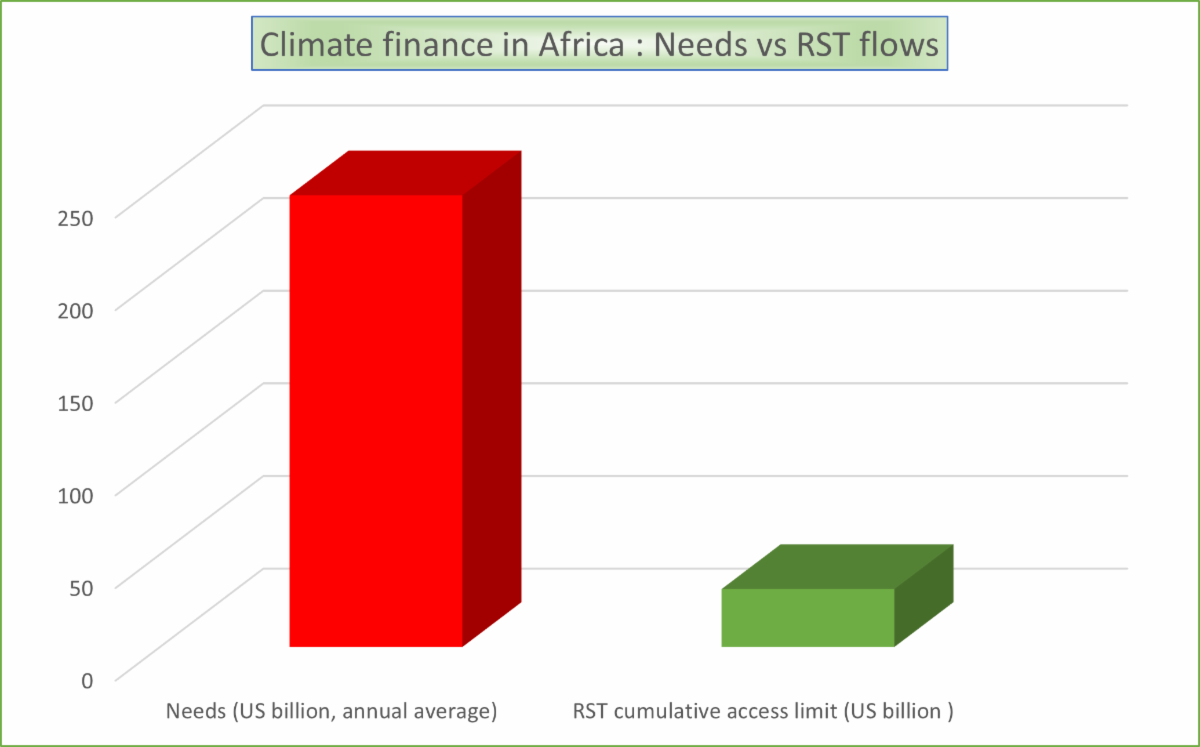

Given that the access ceiling for eligible members is less than 150% of the quota or SDR 1 billion, and the starting point for determining access is an access standard of 75% of the quota member, this facility is far from being able to meet the needs of African countries in terms of climate finance.

Indeed, when we estimate the total access ceiling for all African members eligible for the RST (around USD 31.3 billion), we realize that this amount is extremely low compared to the average annual needs of African countries (USD 243 billion) to cope with the effects of climate change. So even if loans were allocated under the RST every year – which is not the case – and even loans are meant to play a catalytic role, they would not be enough to meet the climate financing needs of African countries.

Rwanda, for example, which has a government-estimated cost for new investments in adaptation projects of USD 11 billion, of which USD 6.9 billion is conditional on new financing, has received only USD 310 million to, among other things, strengthen its resilience to climate change.

The effectiveness of the facility is limited because the loan quota is linked to their SDR quota, which depends on the size of their GDP. Countries with small economies and a significant need for climate finance are not favored.

Beyond IMF Financing

In this new climate reality, African countries need substantial and diversified funding to continue their economic development process. Indeed, the mobilization of additional resources would widen the room for maneuvering of African countries, enabling them to simultaneously meet the challenges of climate change, the pandemic, the economic disruption caused by the war in Ukraine, and long-standing structural obstacles.

Lack of projects

In addition to the need for financing, there is also an absence of shovel-ready projects. Estimates based, inter alia, on Nationally Determined Contributions are largely based on ideas that have not been subjected to a feasibility study.

There is an urgent need to develop a project pipeline before making the case for additional grants today or creating new facilities tomorrow because it is unclear what the actual immediate needs are. In Mauritius, for example, the IMF estimates the need for unfunded shovel-ready projects at $200 million per year.

In this context, in addition to concessional financing, African decision-makers need to explore other sources of financing that may not have been used regularly, such as (1) debt instruments that are linked to climate change, (2) international carbon credit systems, (3) climate-related insurance systems and (4) regional grants from the EU that can only be accessed by several countries working together. Over the medium term, the international architecture will also need to be changed so that the Multi-lateral Development Banks can set up with unused SDRs concessional facilities that complement the RSF.

1. Climate-related debt instruments

Climate-related debt instruments can help limit sovereign debt while promoting adaptation or mitigation efforts.

The benefits of such instruments include better and cheaper reporting and monitoring on the use of funds, reduced transaction costs, and improved public financial management, procurement, and statistics.

They also promote greater transparency and accountability in debt management. These include Green Bonds, debt swaps, and debt relief or cancellation. In the latter case, debt cancellation is linked to specific climate investments or actions.

2. International carbon credit systems

Carbon credits can be used more often by African countries endowed by nature. For example, Gabon could sell units of emissions absorbed by its forest to a private company seeking to offset its emissions. This revenue could be an additional source of financing,

especially for climate-related projects and other development expenditures in the country. However, this system is being called into question by the Paris Agreement.

International carbon credit schemes that simply offset emissions produced elsewhere risk increasing global emissions, which is at odds with the mitigation objectives of the Paris Agreement.

Frameworks such as REDD+ could serve as an alternative to this brake. REDD+ is an emissions reduction framework based on forest and nature conservation.

3. Climate-related insurance systems

Insurance schemes are an important component of risk management, although they are no substitute for investment in physical and financial resilience.

Risk insurance schemes, climate risk pooling, and other insurance solutions can help countries, households, and businesses cope with the consequences of climate-related disasters, providing reliable and rapid support following extreme weather events.

Climate insurance can have a positive impact on beneficiaries’ investment levels and macroeconomic performance. It can also complement targeted social assistance (Surminski, Bouwer, and Linnerooth-Bayer 2016).

For example, farmers covered by climate insurance are more likely to invest in equipment and infrastructure, thereby increasing their productivity and output. To reduce their insurance premiums, beneficiaries can also invest in reducing their exposure to climate risks.

4. Need for Additional Facilities for grants and highly concessional loans

IMF funding has always been catalytic and normally the RSF could be complemented by borrowing from the Multilateral Development Banks and bilateral development partners.

However, when debt service is already stretched and the gap to finance building resilience and sustainability is so large, only grant or highly concessional financing can complement the RSF without raising debt sustainability concerns.

This is why EU grants need to be mobilized in the short run and over the medium term unused SDRs need to be recycled to create RSF-type facilities with the same eligibility criteria at the World Bank and Regional Development Banks.