The global PC market in 2024 was marked by stabilization and ended on the road to recovery and a commercial refresh cycle in 2025.

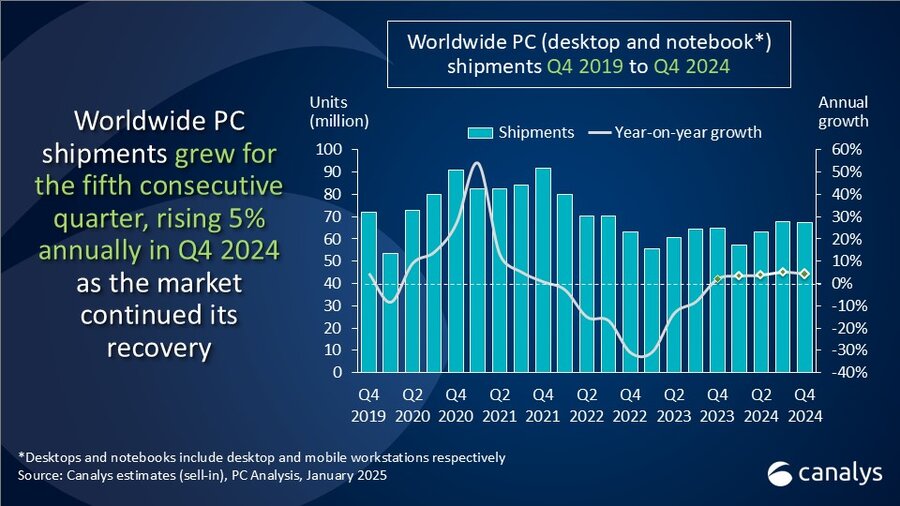

According to the latest Canalys data, the PC market achieved its fifth consecutive quarter of growth in Q4, with total shipments of desktops, notebooks and workstations rising 4.6% to 67.4 million units.

Notebook shipments (including mobile workstations) reached 53.7 million units, growing 6.2%. While desktops (including desktop workstations) shipments fell 1.4% to 13.7 million units.

2025 is expected to be a year of accelerating growth as the Windows 10 end-of-support deadline in October pushes hundreds of millions of PC users to refresh their devices.

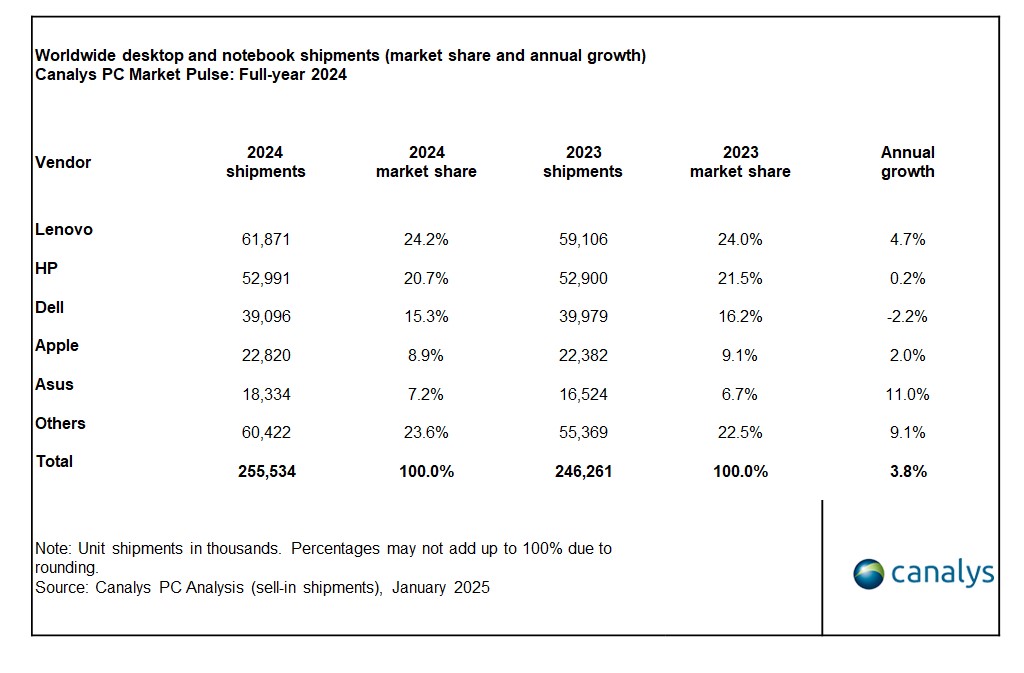

“2024 was a year of modest recovery and a return to traditional seasonality for the PC market as full-year shipments grew 3.8%. Growth increased slightly in Q4, with shipments rising by 4.6% year on year, signaling a positive trend as we moved to within a year of the Windows 10 end-of-support date,” said Kieren Jessop, Analyst at Canalys. “Holiday season demand was supported by strong discounting by vendors and retailers, enticing consumers who have become increasingly price-sensitive. Additionally, the use of buy now, pay later services supported this trend, with increasing examples of these offerings being leveraged to drive spending on big-ticket items, such as PCs. In China, government stimulus in the form of consumer subsidies helped to promote spending on notebooks amid a demand environment that had been weakening.”

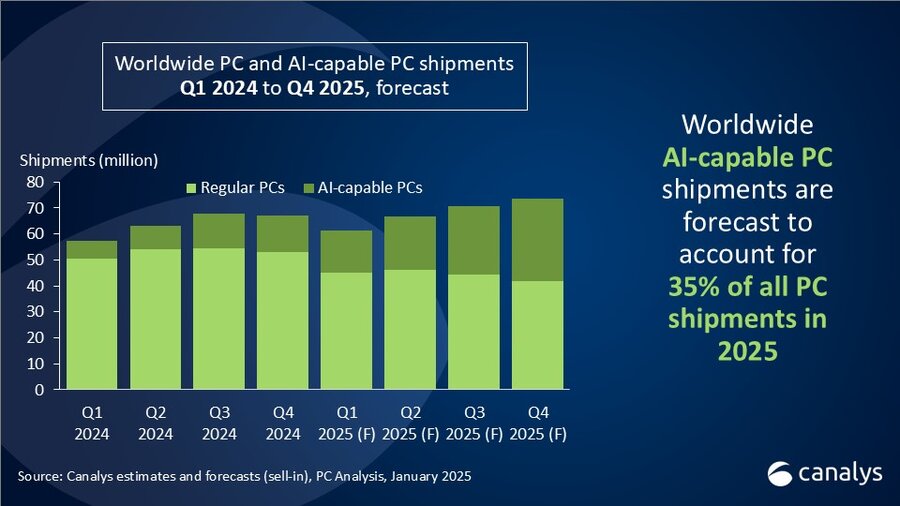

“Looking ahead, the PC market is set for accelerating growth, primarily driven by commercial demand as businesses prepare for the end of Windows 10,” said Ishan Dutt, principal analyst at Canalys. “The advances showcased at CES 2025 highlight the industry’s commitment to making AI-capable PCs a halo category, enticing customers into conversations around a wider fleet refresh. As CPU and PC vendor roadmaps begin to bring on-device AI into more categories, price bands and regions, we anticipate that AI-capable PCs will account for 35% of worldwide shipments in 2025.”

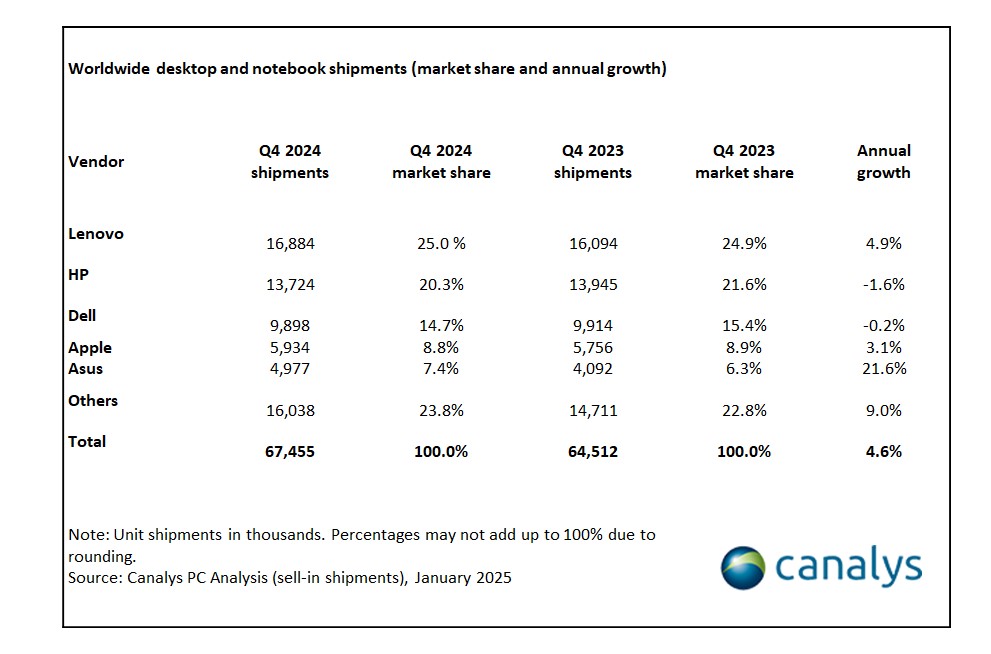

Lenovo took the top spot in Q4 2024, shipping 16.9 million units worldwide, reflecting 4.9% year-on-year growth against an already strong shipment performance in Q4 2023. HP followed in second place with a 1.6% decline in shipments, totaling 13.7 million units globally. Dell held onto third place but declined in every quarter of the year, falling 0.2% in Q4. Apple remained in fourth place, shipping 5.9 million units with 3.1% annual growth, while Asus rounded out the top five, boasting the highest growth among the top vendors with a 21.6% year-on-year increase.