- T2 lost more subscribers than it gained every month since January 2026 – NCC’s MNP data tells the story

When Obafemi Banigbe, chief executive officer of T2 Mobile (formerly 9mobile), stood before an audience at the Marriott Hotel in Lagos in August 2025 and declared that the operator, once Nigeria’s most aspirational telco, would bounce back stronger and sharper, the room applauded.

The narrative was compelling: new ownership, a $3 billion investment plan, a roaming deal with MTN, a four-phase recovery roadmap, and an orange rebrand to bury the green baggage of nine years of decline.

Eight months later, the Nigerian Communications Commission’s Mobile Number Portability data, the most unsparing indicator of whether Nigerians are voting with their SIM cards for or against an operator, is telling a markedly different story.

What the portability data shows

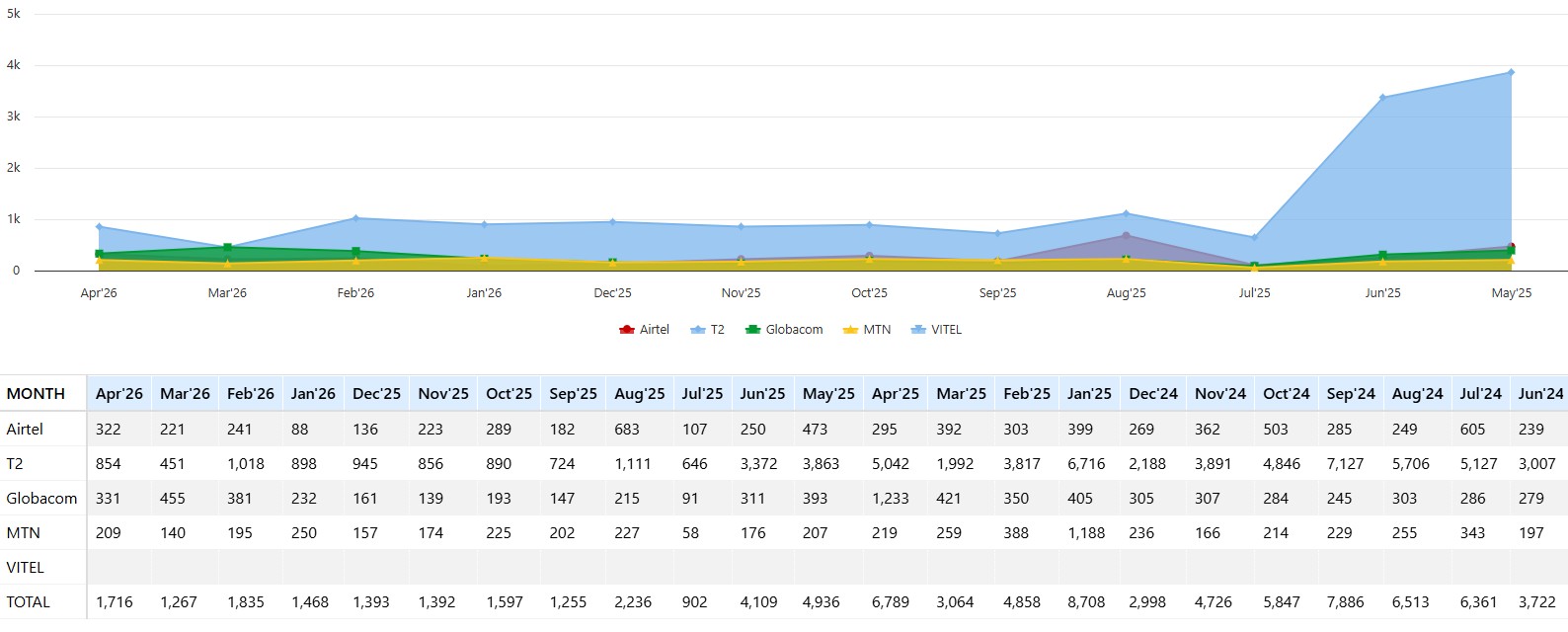

The outgoing MNP figures from Image 1 reveal that T2 has consistently recorded the highest number of subscribers leaving its network across every month tracked in the dataset. In May 2025, T2 lost 3,863 subscribers through portability.

By June 2025, that number had surged to 3,372. The losses moderated through the second half of 2025, dropping to 856 in November 2025 and 945 in December, before a sharp deterioration in early 2026.

February 2026 recorded 1,018 outgoing ports from T2, the highest single-month outgoing figure in the dataset outside of the peak period, before a partial moderation to 451 in March 2026 and 854 in April 2026.

Over the twelve-month period from May 2025 through April 2026 visible in the data, T2’s cumulative outgoing MNP figure towers above every other operator, a pattern that persisted through the rebrand, through the MTN roaming deal announcement, and through every phase of the recovery narrative that T2’s leadership has presented publicly.

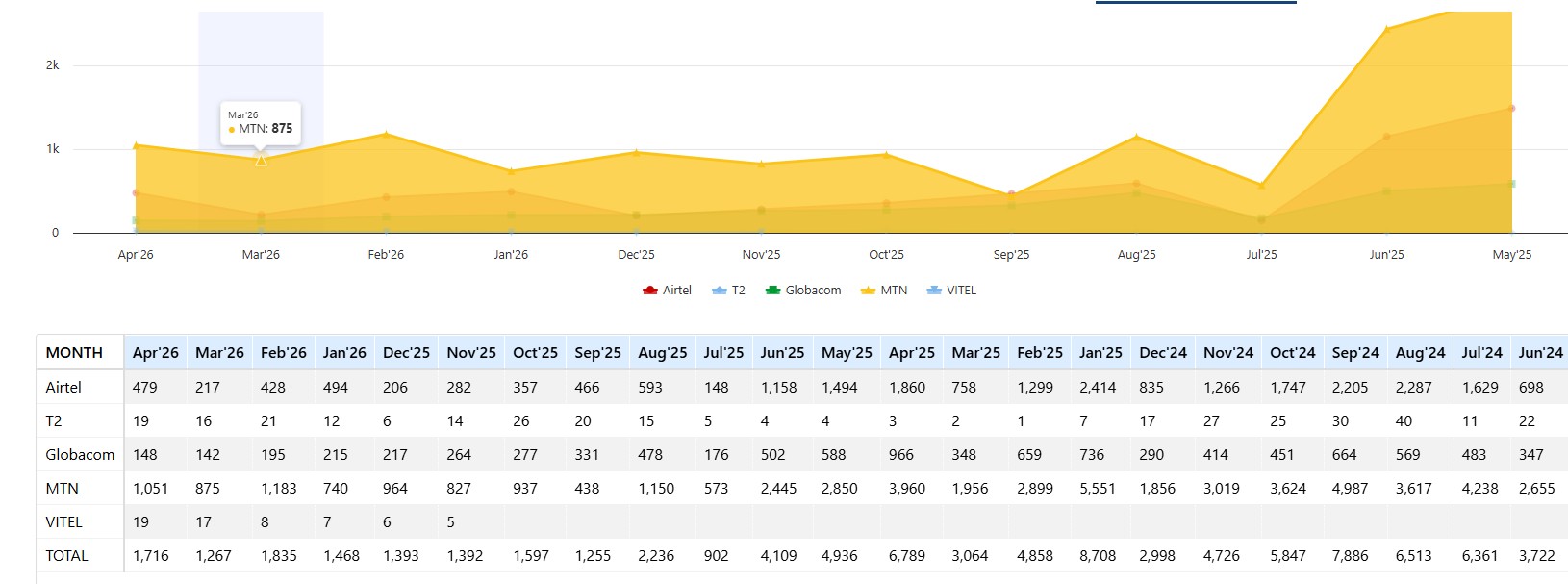

The incoming MNP data in Image 2 provides the other half of the equation, and it confirms the net damage. T2’s incoming port figures are negligible across the entire dataset: single-digit or low double-digit monthly inflows that bear no meaningful relationship to the hundreds of subscribers leaving through outgoing ports in the same months.

In April 2026, the most recent month available, T2 recorded 854 outgoing ports and just 19 incoming ports. That is a net MNP loss of 835 subscribers in a single month. In February 2026, the gap was even more severe: 1,018 outgoing against 21 incoming, a net portability loss of 997.

The arithmetic is unambiguous. For every subscriber T2 attracted through number portability in the period examined, it was losing between 40 and 50.

The CEO’s rebound narrative, and what the data confirms or contradicts

Banigbe’s recovery roadmap was built on four sequential phases: Stabilisation, Modernisation, Transformation, and Growth.

Speaking during a media chat before the rebrand, he was candid about the scale of the challenge.

“The overall infrastructure of the business has really not been upgraded,” he acknowledged. “We are dealing with a lot of obsolete infrastructure, and then we are dealing with a whole lot of issues of declining revenue, declining subscriber base, and costs that are skyrocketing.”

The $3 billion investment plan he unveiled was designed to address precisely those deficiencies, covering network infrastructure refresh, BSS/OSS modernisation through a multi-million dollar partnership with India’s Knot Solutions, a separate multi-million dollar Huawei core network upgrade deal, and the MTN roaming agreement intended to solve the coverage gap that had driven subscribers away for years.

There was a brief moment in late 2025 when the data appeared to validate the narrative. T2 posted its first full quarter of consecutive internet subscriber growth in Q4 2025, adding 9,202 internet users in December to bring its total to 780,237, a modest but notable rebound that suggested the network upgrades and roaming partnership were beginning to gain traction.

But the MNP portability data, which measures something more deliberate than passive subscriber count fluctuation, tells a harder story.

A subscriber who ports out has made an active, considered decision to leave. They have gone through a formal process, obtained a new SIM, and migrated their number to a competitor. That is not churn caused by SIM card expiry or NCC regulatory clean-up. That is a verdict.

Industry analysts examining T2’s portability performance have concluded that while the building blocks of a turnaround may be in place, customer confidence remains fragile.

The continued loss of subscribers through portability indicates that many users are yet to be convinced that the rebrand represents a meaningful shift in service experience rather than a change in name and narrative.

Where the subscribers are going

The incoming portability data in Image 2 identifies precisely where T2’s departing subscribers are heading, and the answer is unambiguous.

MTN is the primary destination, recording the highest incoming MNP figures across almost every month in the dataset: 2,850 incoming ports in May 2025, 2,445 in June 2025, and 1,051 in April 2026, the highest single-month incoming figure of any operator in the most recent reporting period.

Airtel is the second-largest beneficiary, receiving 1,494 incoming ports in May 2025, 1,158 in June 2025, and 479 in April 2026. Globacom captures a smaller but consistent share: 588 incoming in May 2025, 502 in June 2025, and 148 in April 2026.

The pattern confirms that T2’s portability losses are not being redistributed across the market evenly.

They are flowing primarily to the two largest, most infrastructure-heavy operators, a finding consistent with subscriber preference for network quality and coverage reliability over brand differentiation.

The historical context that makes the data more alarming

T2’s portability losses do not exist in isolation. They compound a subscriber decline that began nearly a decade ago.

Etisalat Nigeria peaked at 23.5 million subscribers in 2015 but was forced to rebrand as 9mobile in 2017 after a $1.2 billion loan crisis and the exit of its UAE parent company. Years of underinvestment, network challenges, and failed acquisition attempts led to a massive loss of customers, with subscribers dropping to 2.4 million by June 2025.

The NCC’s 2024 SIM clean-up exercise, which removed inactive subscriptions from the industry’s reported base, hit T2 disproportionately hard.

Globacom and 9mobile were hit hardest, with declines of 69 per cent and 68 per cent respectively, while in one case an operator was found to have overstated nearly 40 million “active” numbers that had generated no revenue for over 90 days.

From 23.5 million subscribers at its peak to a current base estimated below 3 million, T2 has lost more than 87 per cent of its customer base over a decade. The portability data suggests that loss is ongoing, not arrested.

Does the data corroborate the CEO’s rebound claim?

Banigbe’s rebound narrative rests on a specific claim, that infrastructure investment, network refresh, the MTN roaming partnership, and the brand transformation would begin reversing the subscriber exodus. The Q4 2025 internet subscriber data offered a brief, modest validation of that claim.

The MNP data for January through April 2026 does not.

Outgoing ports from T2 in February 2026 reached 1,018, the highest in the dataset outside the peak period, before moderating to 451 in March and rising again to 854 in April.

Across those four months of 2026, T2 recorded a total of 2,612 outgoing ports against just 73 incoming ports, a net portability loss of 2,539 subscribers in the first four months of the year alone.

For a network with a subscriber base already below 3.6 million, which rate of portability loss is not a rounding error. It is a signal that the service quality improvements underpinning the CEO’s rebound narrative have not yet translated into the customer experience that retains subscribers or attracts them from competitors.

Customer frustration remains documented across social media, with complaints about persistent call drops, failed airtime transactions, and delays in receiving one-time passwords, experiences that stand in contrast to the AI-powered, customer-centric vision T2 outlined at its rebrand ceremony.

The four-phase recovery plan: Stabilisation, Modernisation, Transformation, Growth, were never going to deliver visible results overnight. Infrastructure refresh takes time.

Brand perception takes longer. But the portability data is the market’s real-time scoring of whether the transformation is being felt where it matters most: on the subscriber’s handset, in the quality of the call, in the speed of the data connection.

For now, that scoring remains firmly negative. Banigbe said Nigeria always bounces back stronger and sharper. The MNP data says T2 has not yet begun its bounce.