Every Nigerian, whether they know it or not, is a debtor. Not because they took a loan personally, but because the government did on their behalf.

Public debts affect not just those who sit at the negotiating table.

They cut across every aspect, with costs being paid by ordinary Nigerians on a daily basis, including the rising cost of goods and services, limited infrastructure, and other essential services. Every Nigerian is helping to pay even without realizing it.

Breaking down Nigeria’s debt profile

Public debt is the funds that the government, including the federal and state government borrow when expenses exceed revenue.

According to the Debt Management Office (DMO), Nigeria’s public debt had risen to N149.4 trillion in March 2025, equivalent to $97.2 billion. If this figure were split equally among Nigerians, each person would owe about N628,000.

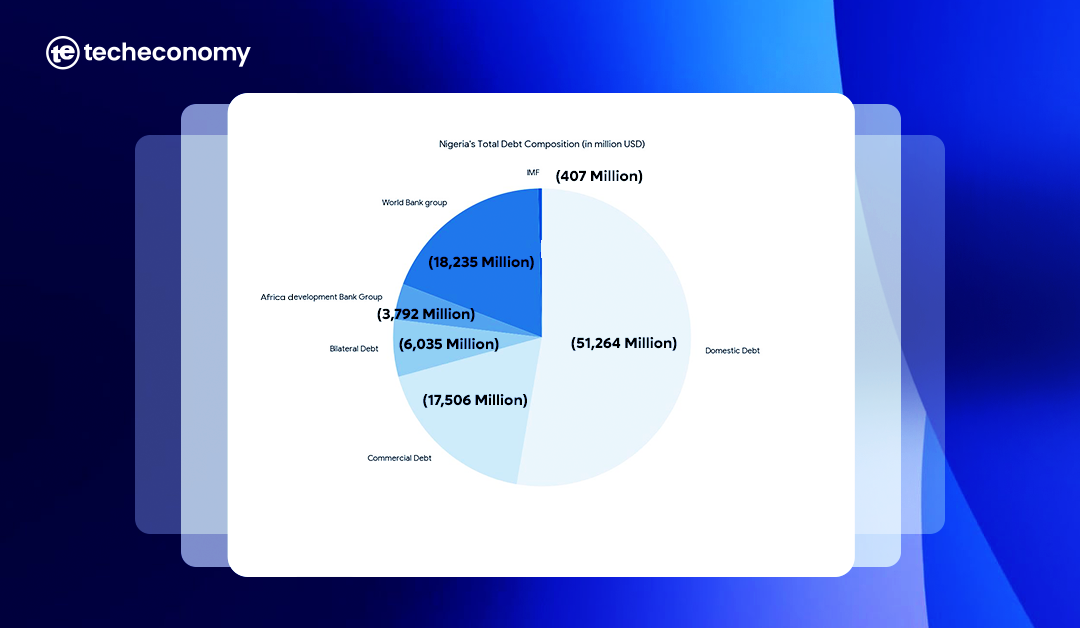

Nigeria’s public debt comprises both external debt (borrowed from foreign lenders like the World Bank, the African Development Bank, and others) and domestic debt (borrowed from commercial banks, pension funds, and investors through bonds and treasury bills).

Data from DMO showed that Nigeria’s total debt comprises 47 percent external debt and 53 percent domestic debt.

Data from the DMO showed that Nigeria spent $1.39 billion in external debt servicing between January to March 2025.

This heavy outflow occurring within three months raises concern about how much is left for investment in infrastructure, health, and education, as the government manages debt obligations along with essential development goals.

Why does Nigeria borrow?

The government borrows to meet development needs, including infrastructure building, improving healthcare, and education.

With oil being the main source of revenue, the fluctuating oil price often has a significant impact on the government’s revenues, and when revenue drops, the government often borrows to fund projects.

Nigeria takes loans to build roads, rails, and other projects that require large upfront spending.

Several factors have contributed to Nigeria’s growing debt over the years, such as reliance on domestic and external borrowing to finance its budget deficits, naira depreciation, worsening cost of servicing external debts, and lack of fiscal discipline.

The loan is often justified as necessary for completing and executing capital projects. However, Nigeria’s borrowing is often used to cover budget deficit, fund recurrent expenses, and service older debts, leading to rising concern about long-term sustainability.

What are the concerns?

According to a recent report by Nigeria Extractive Industries Transparency Initiative (NEITI), debt deductions now consume about 20 percent to 25 percent of some states’ allocation, leaving little for development, paying salaries, and funding government services, leading to abandoned projects, unpaid salaries, more borrowing to pay old debts, and weakening of financial independence.

Nigeria spends an increasing portion of its revenue on servicing loans, leaving less funds for critical development like schools, hospitals, and roads, areas directly affecting the daily lives of citizens.

As Nigeria’s economy is heavily reliant on oil export, a drop in oil prices or production sharply reduces revenue, making it harder to repay debts.

This forces the government to borrow more to meet basic obligations, creating an endless cycle of borrowing and debt servicing.

Loans used to fund non-revenue generating expenses like paying salaries, recurrent expenses, means that young Nigerians and future taxpayers will inherit today’s borrowing without enjoying tangible benefits.

Debt repayments being paid first before any other expenditure, leaves capital projects underfunded or abandoned half way.

Also, domestic loans are expected to fund infrastructure; however, most of the time, it is used to fund expenditure, in addition to the lack of transparency.

To tackle Nigeria’s debt crisis, it is important for the government to boost non-oil revenue, as continuous reliance on oil revenue will continue to affect the country’s revenue as oil prices fluctuate, leading to more borrowing.

Prioritize borrowing for projects with measurable returns like infrastructure development, industrial projects that create jobs and grow GDP, while ensuring loans are used for intended objectives.

As more funds are allocated to debt servicing and interest payments, it chips away at funds meant for schools, roads, and critical projects.

Unless borrowing is matched with bold reforms and real investment returns, today’s quick fixes could become tomorrow’s chains, binding future generations to obligations they never agreed to.