Writer: MICHAEL OGWUDE

Blockchain, introduced in 2008, has been a total game-changer worldwide, especially in the financial sector. It’s like a superhero swooping in to solve the financial problems countries grapple with.

One highlight of blockchain is its ability to tackle cross-border remittances, making financial transactions between countries seamless. It’s like a magic wand waving away the complexities of international money transfers.

Cross-border remittances are essential for developing economies to engage in foreign trade and other financial activities with neighboring and foreign countries.

In line with this, blockchain, a secure, fast, and transparent way of performing financial transactions, is being leveraged by developing economies to grow even faster.

Overcoming Challenges with Blockchain: Efficiency Through Decentralization

Former CEO of Digital Asset Holdings – Blythe Masters, a popular blockchain adherent, said in a speech, “Blockchain is going to revolutionize the way we do business.”

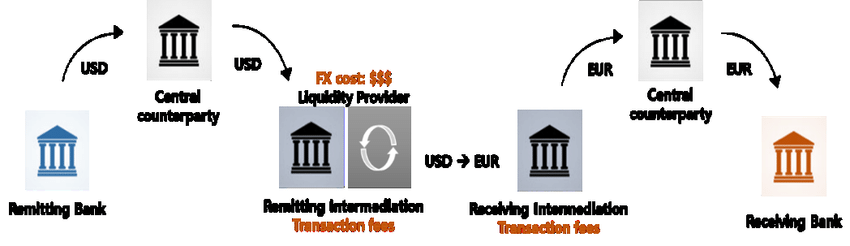

Before the creation and utilization of blockchain, the financial sector was very much centralized. In cross-border remittances, there is usually an intermediary or, in some cases, more than one, which is costly to those developing economies. Besides the cost, there was also a delay in the transaction process. Blockchain, through cryptocurrencies, for example, makes cross-border remittance easier with peer-to-peer (P2P) transfers, a payment made by individuals with different accounts directly to each other with the help of the internet. This takes out the stress faced by individuals and companies, in waiting for their local banks to process transactions, saving both cost and time.

Economic Empowerment and Financial Engagement

Blockchain helps economically developing countries easily engage in international trade. Most individuals in such countries do not have access to traditional banking systems, making them non-participants in economic activities they should typically have access to.

Since blockchain allows for internet banking through P2P and various other transfer means, these individuals can put their mobile phones to good use. Blockchain can help them perform in the financial system because there are not many barriers, and thanks to smartphones, making improved financial choices bolsters well-being.

Limitation of Error

Unlike traditional cross-border remittances, blockchain reduces errors during transactions. Traditionally, an error may occur due to multiple intermediaries, leading to transaction delays and frustration.

However, with blockchain, transactions can, with ease, be settled. This is because it offers a secure and precise technology that blocks any error, unless made from the individual’s side. The process used by blockchain technologies is fast and transparent; the parties involved in the transaction are sure there can be no manipulation once the transaction is in progress since it is direct.

Conclusion

As global transformation occurs, more developing countries are starting to accept blockchain through cryptocurrencies like BTC, Ripple, and Ethereum. As a result of this, developing economies can catch up with those ahead of them and enjoy all the benefits that come with it, including efficiency, security, and affordability.

Nothing comes with ease. Developing economies must know that in adopting blockchain for cross-border remittances, adequate provision must be made to accommodate growth.

The improvement of technological output in such countries is one means, another is the provision of sufficient information about blockchain and its advantages in financial transactions. Lastly, such economies’ governments should have better regulations guiding blockchain networks.