- 2% of Nigeria’s unbanked poor indicated their preference for saving their money in a safe place at home or carrying it around, indicating that more than 50% of this segment of the population could lose their savings if they are unable to exchange old notes for new notes.

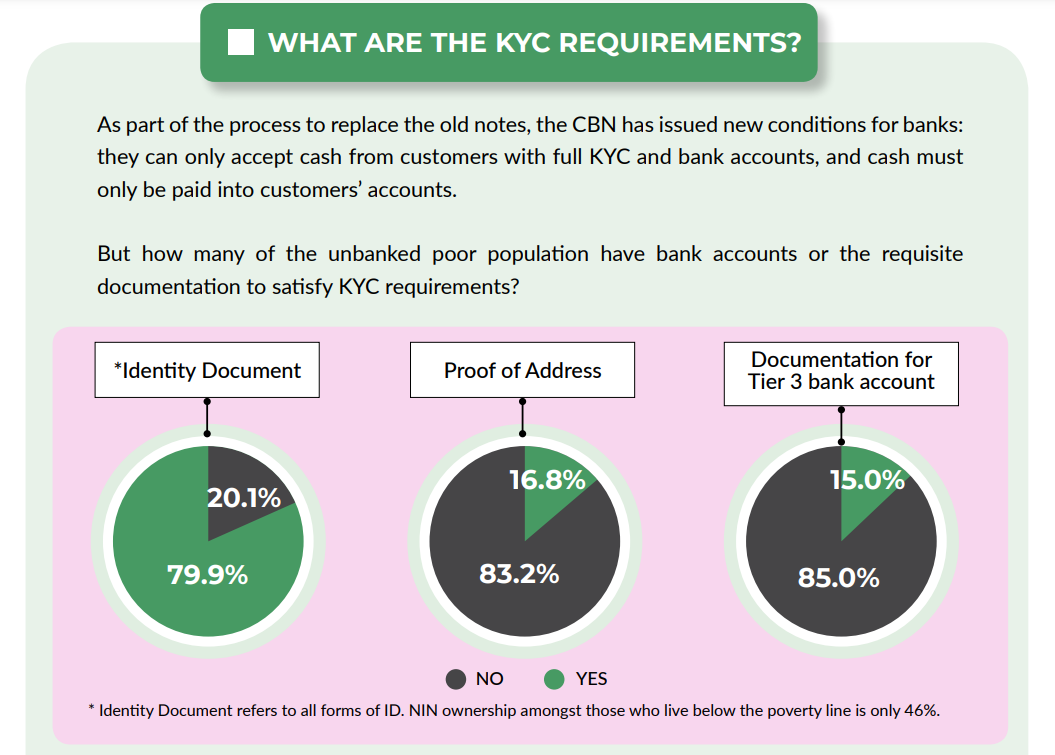

- The requirement by the CBN for individuals to have full KYC and deposit their old notes in a bank account could adversely impact the un(der)banked segment of Nigeria’s population who are unlikely to own a bank account or have the requisite documentation for KYC.

- The ability of financially excluded Nigerians to meet the KYC requirements in the timeframe provided and given the barriers to identity ownership will be constrained, and so even if they seek to use the opportunity to enter the formal system, they are likely to face challenges.

The Inclusion for all Initiative, a multifaceted advocacy programme that seeks to address the barriers that prevent the financial and economic inclusion of Nigeria’s poorest and most vulnerable communities, Friday released new data insights on its open source data visualisation platform at the website / https://www.inclusion-for-all.org.

The data suggests that Nigeria’s most vulnerable groups could be adversely affected by the decision to require the exchange of old Naira notes for new notes through an existing bank account.

On 25 October, the Central Bank of Nigeria (CBN) announced plans to redesign the 200, 500 and 1000 naira notes to take effect from 15 December, 2022.

While circulation of the newly designed notes will begin from 15 December, both new and existing notes will remain in circulation until 31 January 2023.

ALSO READ: Naira Redesign will Affect the Poor, SMEs — World Bank

Chinasa Collins-Ogbuo – Head of the Inclusion for all Initiative said: “While we commend the Central Bank for its commitment to the digitisation of Nigeria’s financial services sector, we have to design policy to ensure that it is suitable for the most vulnerable parts of society.

“According to the 2020 EFInA Access to Finance (A2F) Survey, there are more than 38 million Nigerians without a bank account, and our research indicates that more than 50% of these people prefer to save in cash.

“Unbanked Nigerians face a range of barriers to enter the financial system, from access to identity, a lack of proximity to financial access points and a lack of trust in the system. These barriers must be considered and addressed in the Naira redesign process if we are to ensure that this process supports financial inclusion, and does not further marginalise already vulnerable communities.”

The CBN has acknowledged concerns around vulnerable populations, and prioritised banking agents to help those in rural/underserved areas to deposit cash.

However, agents are concentrated in urban areas – far away from vulnerable populations. With a 20% agent coverage target for the northern regions, the North East is only at 6.3%, with North Central at 15.5 % and North West at 12%. Challenges cited include insecurity, distance, lack of electricity, and low profits.

Speaking on the Inclusion for all podcast on the Naira Redesign Professor Yinka David-West, Associate Dean, Lagos Business School said: “From the supply side, we need to ask, ‘Is this a push or pull initiative?.’ I’ll compare the naira redesign to the NIN registration, which was a push directive. All that is required is linking the NIN to a SIM and BVN to facilitate bank transactions. Many Nigerians treasure their phones more than their bank accounts. How can we incorporate seamless banking to fit the lifestyle of Nigerians? Through the naira redesign, the CBN is promoting a cashless system with secure and seamless transactions as a means to facilitate financial inclusion.” To listen to the full podcast please visit the Inclusion for all website or click here.

The Inclusion for all initiative has released a comprehensive snapshot of its research findings, which can be found on the website, or by clicking here.

The snapshot includes a number of recommendations for action to ensure that vulnerable populations are able to participate and secure the associated benefits of access to digital financial services.

- The extension of the time period to exchange Naira notes should be seriously considered in order to enable:

- A rapid and intensified rollout of a sensitisation programme amongst vulnerable groups, informing them of the process, deadlines and requirements.

- To adequately equip, incentivize and capacitate mobile agents to be able to reach and cover people in hard-to-reach areas effectively.

- The extension of existing enrolment locations for NIN and BVN to ensure that vulnerable populations without the documentation for basic KYC are able to secure it prior to the deadline.