Quick Read:

- Driven by premium devices from OEMs such as Apple, Samsung, Google and Huawei, satellite connectivity will reach 46% of the smartphones shipped globally in 2030.

- Proprietary solutions will drive the market in the near term as 3GPP NTN faces challenges around ecosystem readiness.

- The lack of killer use cases is limiting the growth of the 3GPP Release 17-based satellite smartphone market. Release 19 will likely enable broader mid-tier adoption.

- North America leads in global adoption, driven by early investment from telecom operators, satellite operators and smartphone OEMs.

- Qualcomm leads among satellite Android chipset vendors, while MediaTek, Samsung, Google and HiSilicon are increasing competition and accelerating mass adoption.

Satellite connectivity in smartphones is entering a critical growth phase, with NTN-capable devices projected to account for 46% of global smartphone shipments by 2030, according to Counterpoint Research’s latest Smartphone Satellite Connection Report.

Proprietary solutions will drive the market in the near term as 3GPP NTN faces challenges around chipset readiness, operator certification and service maturity.

Apple was the first mainstream smartphone brand to offer satellite connectivity by partnering with Globalstar for the iPhone 14 in 2022.

The recent acquisition of Globalstar by Amazon provides immediate scale and opens up a new revenue stream for Amazon around connectivity-as-a-service.

Huawei was the second player to bring satellite connectivity to smartphones in 2023, and now more than 10 brands are offering it in smartphones.

Commenting on the smartphone OEM dynamics, Soumen Mandal, principal analyst said,

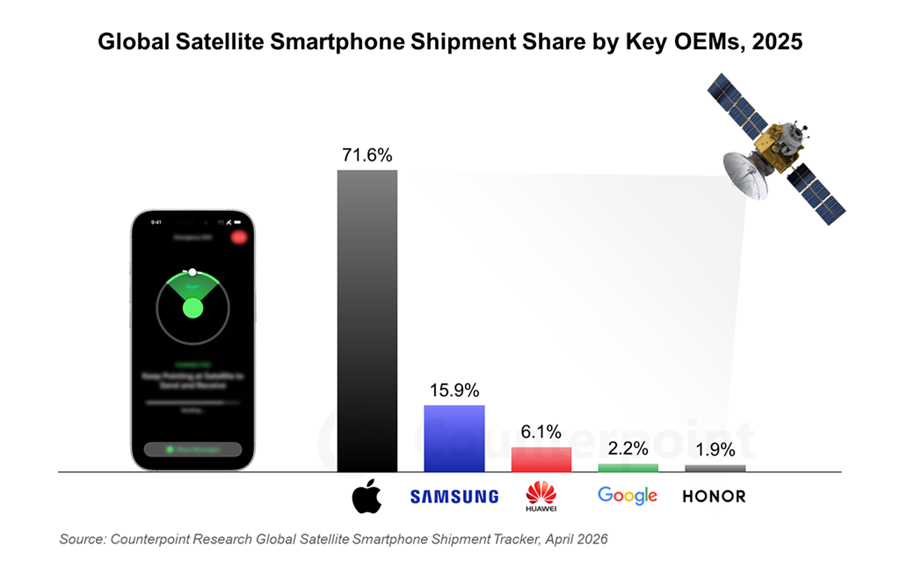

“Apple remains the leading smartphone OEM in terms of NTN-capable smartphone shipments, while Samsung leads the Android ecosystem. Similar to Apple, Huawei and Google follow the proprietary NTN approach. Other Android players, including Samsung, Xiaomi, OPPO, HONOR and vivo, have aligned with 3GPP NTN to enable broader scalability and interoperability.”

The satellite smartphone market is mostly driven by the premium segment, but the lack of killer use cases is limiting mass adoption. 3GPP Release 17-based use cases are limited to SOS and messaging. While 3GPP Release 18 will help further adoption across brands in the premium segment, mass adoption in the mid-price segment is expected only with Release 19.

Commenting on the satellite smartphone SoC market competitive landscape, Shivani Parashar, senior analyst said,

“Qualcomm has been at the forefront among Android chipset players in enabling satellite connectivity through its Snapdragon X80 and X85 modems, followed by Huawei, Google and Samsung. MediaTek is also advancing NTN integration through its MT6825 5G SoC. More participation from chipset players will increase competition while potentially helping scalability.”

The partnerships entered into by North American telecom players, such as T-Mobile with SpaceX, AT&T with AST Mobile and Rogers with SpaceX, along with Apple’s tie-up with Globalstar, have helped bring satellite connectivity to smartphones, making North America an early leader in the field. Though telecom operators in other regions, like Europe and China, are not rushing to offer satellite connectivity, satellite operators are increasing capacity to cater to the mass market.

Commenting on the satellite smartphone market outlook, Peter Richardson, research vice President said,

“Nearly one in two smartphones is expected to support satellite connectivity by 2030. Apple, Google and Samsung will lead in terms of overall penetration, but Android brands targeting the entry and mid-price segments will see less penetration. Satellite offerings by more Android players and telecom operators beyond developed markets will play a key role in accelerating global adoption.”

The satellite smartphone connectivity space is expected to create opportunities across the entire ecosystem, including smartphone OEMs, SoC vendors, component players, telecom operators and satellite operators.

Beyond this, it will also unlock new service models and bundled offerings, where companies like Amazon could integrate satellite connectivity into platforms such as Amazon Prime to enhance the overall consumer experience.

However, the pace of growth will depend on the collaboration of ecosystem players to solve issues such as design and cost constraints, limited use cases, regulatory complexities and network immaturity.